- Key Takeaways

- A Monday Morning, An SMS, And A Bit Of Panic

- What Section 143(1) Actually Checks?

- ITR Processing Timeline: Old VS New Tax Act

- Provide your feedback on BizChat

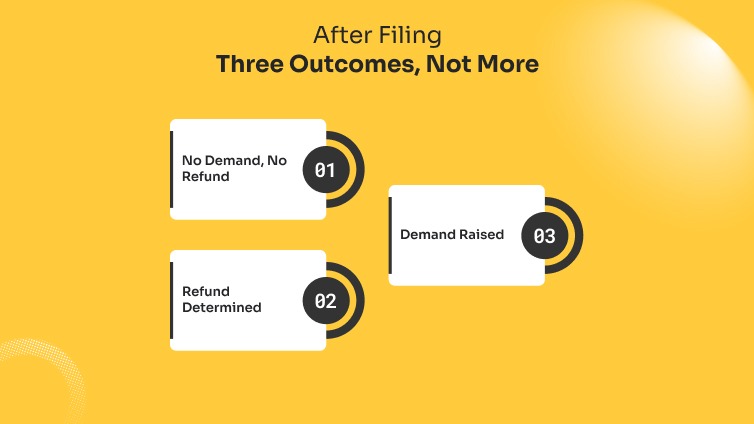

- After Filing: Three Outcomes, Not More

- No Demand, No Refund

- Refund Determined

- Demand Raised

- Why Beginners Usually Get This Notice

- If you're salaried, filing your first or second return:

- If you also have non-salary income like freelancing, a small portfolio, or rent:

- Reading The Intimation Without A Headache

- Once it's open, check three things:

- Comparing 143(1) With The Other Notices

- A Side-By-Side Comparison

- Should You Actually Worry?

- A Simple Four-Step Plan

- Frequently Asked Questions

Income Tax Intimation Under Section 143(1): Why That CPC Email Isn’t the Scary Notice It Looks Like

| What Is Income tax intimation section 143(1)? (Quick Answer) Income tax intimation section 143(1) is an automated communication sent by the Income Tax Department after processing your return. It compares your reported income, deductions, and taxes paid with the department’s records (Form 26AS and AIS) and shows one of three outcomes: no change, refund, or tax demand. |

Key Takeaways

- Income tax intimation section 143(1) is a fully computerised check, not a scrutiny notice.

- It must be sent within 9 months from the end of the financial year in which you filed your return.

- There are only three possible outcomes: no demand, refund, or demand.

- To satisfy a technical reviewer or a chartered accountant, explicitly state that the intimation itself is deemed to be a notice of demand under Section 156. The 30-day clock starts immediately.

- If you’re filing for FY 2025-26 (AY 2026-27) right now, Section 143(1) of the old law applies in full. The new Income-tax Act, 2025 doesn’t touch this year’s return.

| What Section 143(1) Checks And What It Doesn’t? What it does: Matches your income with Form 26AS and AIS Verifies TDS and tax payments Corrects arithmetic errors in your return Flags missing income already reported to the department What it doesn’t do: It does not verify your investment proofs It does not audit your expenses or deductions deeply It does not mean your return is under scrutiny It does not involve a human officer reviewing your case Check out the differences properly. For most people, this turns out to be just a system-level reconciliation, not an investigation. |

A Monday Morning, An SMS, And A Bit Of Panic

Ritika, a 27-year-old content writer in Pune, filed her ITR in July 2026 and got on with her week. Three months later, an SMS landed:

“Your ITR for AY 2026-27 has been processed. Intimation sent to your registered email.”

Her stomach dropped a little when she saw the message.

It didn’t need to. The password-protected PDF showed the department’s numbers matching hers almost exactly, except for one line:

₹420 of savings account interest she’d genuinely forgotten to report. The correction will barely increase her refund value. And reading the PDF took her about ten minutes.

This is roughly how it plays out for most salaried Indians. It isn’t a punishment or proof that you did something wrong. On the contrary, it’s the routine final step of filing.

What Section 143(1) Actually Checks?

Once you e-verify your ITR, it is sent to the Centralized Processing Center (CPC) in Bengaluru, where no officer reads it line by line. An algorithm runs the comparison instead.

That means your figures against your Form 26AS, your Annual Information Statement (AIS), the TDS your employer or bank already reported, and the arithmetic in your own return.

It fixes maths errors, disallows a deduction with no matching entry, and lines up what you owe against what you’ve already paid.

That’s the full extent of it. It doesn’t examine whether your claimed expenses are genuine or whether your investment proofs would withstand closer scrutiny.

That deeper check, if it ever happens, falls under a different section entirely.

ITR Processing Timeline: Old VS New Tax Act

The processing timeline is precisely nine months, counted from the end of the financial year in which you filed the return, not the year your income belongs to.

Under the 9-month rule from the end of the financial year in which it was filed, if you file in July 2026 (which falls in FY 2026-27), the financial year ends on 31 March 2027.

Counting 9 months from there means the deadline is 31 December 2027. Your math is 100% correct here!

However, verify your phrasing to ensure you clearly mention that the 9 months start from the end of that filing financial year (March 31, 2027)

Meanwhile, there is no second chance for people who miss that window. In other words, your ITR-V acknowledgment becomes the final word.

This is also where much of the recent confusion comes from. The new Income-tax Act, 2025 came into force on 1 April 2026. Meanwhile, it applies only to income earned from FY 2026–27 onward.

Provide your feedback on BizChat

That’s what the new law calls “Tax Year 2026-27.”

Your FY 2025-26 return runs entirely under the old Section 143(1), exactly as it always has.

Once the new Act fully takes over, the equivalent provision will carry a different number, Section 270(1), with the same nine-month logic. That’s a question for next year’s filing, not this one.

| [File ITR: July 2026] ↓ [Filing Year Ends: 31 March 2027] ↓ (9-Month Window) [CPC Deadline: 31 December 2027] |

After Filing: Three Outcomes, Not More

Open the intimation, and you’ll land in exactly one of three buckets.

No Demand, No Refund

Your numbers and the department’s agree. In other words, there is nothing to pay, and nothing coming back. Simply put, file the email away and move on.

Refund Determined

You paid more than you owed, usually through excess TDS. Refunds under ₹100 aren’t issued separately; anything above that amount is credited to your bank account, provided you pre-validate it on the e-filing portal.

Demand Raised

The system found a gap. For example, there is an:

- Undeclared interest

- A disallowed deduction

- A maths error that had worked in your favor.

This is also where the phrase “income tax demand notice 143(1)” comes from: when the intimation shows tax payable, it doubles as a notice of demand under Section 156, and the 30-day window to respond begins on the day it’s served.

| Outcome | What It Means | What You Should Do |

|---|---|---|

| No Demand, No Refund | Your return matches the department’s records | Nothing, just keep a copy for your files |

| Refund Determined | You overpaid tax (commonly, excess TDS) | Confirm your bank account is pre-validated, then wait |

| Demand Raised | A mismatch increased your tax liability | Check the reason code; pay within 30 days, or file a rectification |

Why Beginners Usually Get This Notice

The reasons tend to cluster by the kind of return you filed.

If you’re salaried, filing your first or second return:

- Savings or fixed deposit interest wasn’t added under “income from other sources,” even though your bank had already reported it.

- You switched jobs mid-year, and the second employer’s Form 16 was never combined with the first. Therefore, the total TDS doesn’t match the total income.

- A deduction under 80C or 80D was claimed, but the attached entry didn’t match the requirements.

If you also have non-salary income like freelancing, a small portfolio, or rent:

- A round figure replaced an actual number somewhere, creating a small arithmetic gap.

- Capital gains from a mutual fund redemption were left out because the statement arrived after filing.

- A loss from an earlier year couldn’t be carried forward because that year’s return missed its due date.

None of this means anyone did something dishonest. Most of it is a simple timing gap between what you knew when you filed and what the department’s systems already had on record.

Reading The Intimation Without A Headache

The PDF is password-protected: your PAN in lowercase, followed by your date of birth in DDMMYYYY format, no spaces. PAN ABCDE1234F with a birth date of 5 March 1998 opens with abcde1234f05031998.

Once it’s open, check three things:

- The acknowledgment number, which should match your ITR-V

- The side-by-side columns comparing “as provided by you” against “as computed under section 143(1)”

- Finally, the final line showing refund or demand.

Wherever a number changed, a reason code sits beside it. Again. That is usually enough to tell you whether to accept the change or push back.

Comparing 143(1) With The Other Notices

Section 143(1) isn’t the only letter the department sends. On the contrary, it iss just the one nearly everyone gets, since every processed return generates one.

Even if it only confirms there’s nothing to discuss.

A section 142(1) income tax notice works differently. It’s usually issued before assessment, asking you to file a return you haven’t submitted yet or to produce specific documents, and ignoring it carries real consequences.

Among the income tax notices salaried individuals most often see, 143(1) is the routine, automated one.

On the other hand, a 142(1) notice, or scrutiny under 143(2), is rarer and means a human at the department wants something specific from you.

A Side-By-Side Comparison

| Feature | Section143(1): Intimation | Section 142(1): Inquiry Notice | Section 143(2): Scrutiny Notice |

|---|---|---|---|

| Primary Purpose | To provide an automated summary of your processed ITR, highlighting any mathematical errors or TDS mismatches. | To request additional documentation, account books, or clarifications before an assessment is finalized. | To notify you that your tax return has been selected for a detailed, manual audit by a tax officer. |

| Who/What Triggers It | Automated Centralized System: Generated entirely by the CPC algorithm in Bengaluru. | Assessing Officer (AO): Issued manually by a human officer handling your local jurisdiction. | Assessing Officer / National Faceless Assessment Center (NFAC): Triggered by risk-assessment algorithms. |

| When It Is Sent | After Filing: Once your tax return is successfully processed. | Pre- or Post-Filing: Usually sent if you missed a filing deadline or if the initial data looks incomplete. | After Filing: Sent if your return exhibits high-risk tax indicators or massive income variances. |

| What It Requires From You | Conditional Action: Nothing if your records match. If a demand is raised, you must pay or file a rectification within 30 days. | Compulsory Response: You must provide the requested bank statements, rent agreements, or expense bills. | Mandatory Legal Defense: You must submit comprehensive legal and financial proofs to validate your return. |

| Risk / Anxiety Level | Very Low: It is a routine administrative reconciliation sent to nearly every taxpayer. | Moderate: It is an information gathering request. Providing accurate documents typically closes to the matter. | High: Your file is undergoing a formal tax audit. Ignoring this notice leads to best-judgment tax assessments. |

| Penalty for non-compliance | Accumulation of monthly statutory interest on unpaid tax demands. | A flat penalty of ₹10,000 per failure, alongside potential prosecution under Section 276D. | Rejection of your declared figures, hefty tax penalties, and an automated reassessment of your total income. |

Should You Actually Worry?

No, not about the intimation itself. Worry only if it shows a demand you disagree with, and you let the 30 days run out without responding.

It’s just two sets of numbers being reconciled, and most of the time, they’re already close.

A Simple Four-Step Plan

- Read the comparison columns first. Don’t jump to the final number. On the contrary, find where the difference actually came from.

- Cross-check against Form 26AS and AIS. Most gaps trace back to a TDS entry or an interest figure already in place.

- Decide: accept or rectify. If the department’s version is correct, pay it or accept the refund. If you’re confident, you’re right, file a rectification under “Services > Rectification” on the e-filing portal. Remember that the “tax credit mismatch” is the reason most people end up choosing.

- Keep the PDF. You’ll need the acknowledgment number again for any future rectification or conversation with a tax professional.

Tax professionals tend to flag one mistake more than any other here: letting a small demand remain unpaid because it feels too minor to matter.

Interest accrues monthly, and an unresolved demand can quietly be applied against a refund you’re owed later.

Frequently Asked Questions

No. It’s a fully automated comparison. A scrutiny notice comes later, under a different section, and involves an actual assessing officer examining your case in depth.

If nine months have passed since the end of the financial year in which you filed and nothing has arrived, the department treats your original ITR-V acknowledgment as the final intimation. Your return stands accepted as filed.

Occasionally, yes! Usually, because a TDS entry hadn’t been updated in the department’s system yet. Checking your Form 26AS before reacting usually clears this up quickly.

Not always. Straightforward mismatches can be rectified online by yourself. If the demand involves a disallowed deduction you’re confident is valid, professional help is worth the cost.

Interest accrues each month, and the department can eventually apply the amount to any refund you’re owed later or initiate recovery action.

Disclaimer: This article explains the general process under Section 143(1). For advice specific to your own return, a chartered accountant can review your actual numbers.

Share this article: