- Key Takeaways

- The Notice That Showed Up Out Of Nowhere

- What Is Section 142(1)? A Simple Breakdown

- Characteristics Of A Section 142(1) Notice

- Who Gets This Notice And Why?

- Group 1: Non-filers.

- Group 2: Filers With Gaps.

- The Components Of The Section 142(1) Income Tax Notice

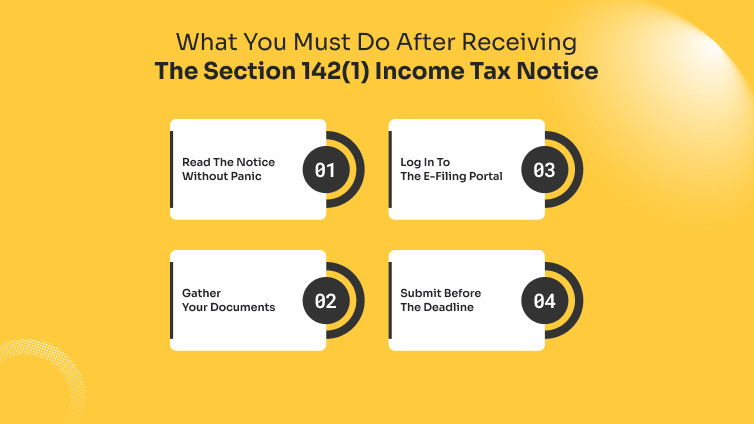

- What You Must Do After Receiving The Section 142(1) Income Tax Notice

- Step 1: Read The Notice Without Panic

- Step 2: Gather Your Documents

- Step 3: Log In To The E-Filing Portal

- Step 4: Submit Before The Deadline

- Pros And Cons Of Responding Promptly

- Pros Of Responding Promptly:

- Cons Of Ignoring Or Delaying:

- What Happens If You Don't Respond To The Section 142(1) Income Tax Notice

- Should Beginners Worry About This Notice?

- Common Mistakes To Avoid

- Section 142(1) VS. Other Notices: The Key Differences

- A Simple Framework For Handling Any Tax Notice

- Solving Common Queries And Confusions Of Tax Filers

- Can A Section 142(1) Notice Be Issued Even If I Already Filed My Return?

- Is There A Time Limit For Issuing This Notice?

- What If I Don't Agree With What The Notice Is Asking?

- Can I Respond Myself, Or Do I Need A CA?

- What Is A Faceless Assessment?

- Will This Notice Show Up On My Credit Report?

- What If I Need More Time To Respond?

Got That Section 142(1) Email? Here’s the No-Panic Way to Deal With It

A Section 142(1) income tax notice is an official letter from the Income Tax Department asking you to either file a pending return or share documents that the Assessing Officer needs to complete your assessment.

This is not a raid notice or any sort of conviction. But should you worry if you receive the 142(1) notice?

In most cases, no. Usually, it is manageable. However, you must know how to act. The protocol for reciprocating when you receive a section 142(1) income tax notice is very important!

Key Takeaways

- Section 142(1) is an inquiry notice, not a tax demand

- You get it when you haven’t filed your ITR, or when the officer needs more details

- Ignoring it can cost you ₹10,000 per instance as a penalty

- All responses go online through the Income Tax e-filing portal; i.e., no office visits needed

- The AO generally cannot ask for documents older than 3 years in standard cases

The Notice That Showed Up Out Of Nowhere

How can the section 142(1) income tax notice impact you? Let’s try to understand that with an example.

Priya is a 26-year-old marketing executive from Bengaluru. She started a recurring deposit, redeemed some mutual funds mid-year, and also did a short freelance project worth ₹40,000.

Therefore, she filed her ITR. But in a hurry, she forgot the freelance part. Two months later, she got an email from the Income Tax Department. The subject line read:

“Notice u/s 142(1) of the Income Tax Act.”

Her stomach dropped. She forwarded it to her father, who said, “get a CA fast.” A colleague said it probably meant a tax raid. Another friend said it was just a formality.

So what did Priya actually go through? Above all, she became confused. Most importantly, she did not know what to do or not to do afer hearing so much conflicting advises.

But Priya is not someone exclusive. Every year, many people face situations like hers. What’s worse, most of them don’t know that they can easily resolve this issue. That’s what I am going to discuss here.

What Is Section 142(1)? A Simple Breakdown

Section 142(1) of the Income Tax Act, 1961, gives the Assessing Officer (AO) the legal authority to ask you for information before finalizing your tax assessment. The AO is a government official whose job is to verify that your filed return is accurate and complete.

Under this section, the AO can:

- Ask you to file your ITR if you missed the deadline

- Ask for specific documents or books of accounts to verify income or deductions

- Require you to provide a written explanation about certain financial transactions

That’s the whole thing. In simpler words, it is an inquiry. Nothing more than that.

Characteristics Of A Section 142(1) Notice

Before doing anything, understand what this notice looks like:

- It is issued in writing by the Assessing Officer. Again, it is never just a phone call or WhatsApp message

- The government sends it to your registered email and e-filing portal account at incometax.gov.in

- The notice lists specific documents or details required. To clarify, it cannot be a vague “send everything” demand

- Comes with a response deadline, usually 15 to 30 days

- Mentions consequences for non-compliance if you ignore it

If you receive an income-tax-related message asking for bank account details or OTPs, that is a scam. That is to say, legitimate 142(1) notices always appear in your e-filing account under “e-Proceedings.

Who Gets This Notice And Why?

Two broad groups of people usually receive a Section 142(1) notice.

Group 1: Non-filers.

You were required to file an ITR but didn’t. The AO is sending this notice to ask you to file immediately. Even if your income was below the taxable limit in a particular year.

However, it is not random. Certain conditions make the tax office send the notice.

For example, having foreign assets or high bank credits can still require filing. Financial advisors always recommend filing on time just to avoid this situation.

Group 2: Filers With Gaps.

You filed your ITR, but there are discrepancies. In that case, you can also get a 142(1) notice. Here are the most common discrepancies that the Income Tax department flags:

- Cash deposits above ₹10 lakh that don’t match declared income

- Capital gains from mutual fund or share sales that weren’t reported

- Large deductions claimed without proper supporting documents

- Freelance or rental income that platforms or tenants may have reported to the department

In Priya’s case, her freelance platform had made payments that were flagged through the Annual Information Return (AIR). The AO noticed the mismatch and issued the notice.

The Components Of The Section 142(1) Income Tax Notice

| Component | What It Contains |

|---|---|

| Taxpayer Details | Your name, PAN, and registered address |

| Assessment Year | The financial year under examination |

| What Is Being Asked | Specific documents, written clarifications, or unfiled return |

| Response Deadline | Usually 15 to 30 days from the date of the notice |

| Consequences | Penalties and assessment implications for non-compliance |

Pro Tip: There is no fixed outer time limit for issuing this notice under the law. The AO can issue it even after the relevant assessment year ends. However, in most standard cases, documents older than three years cannot be demanded.

What You Must Do After Receiving The Section 142(1) Income Tax Notice

Here is a step by step action plan. Follow these steps appropriately, when you receive the section 142(1) income tax notice:

Step 1: Read The Notice Without Panic

Open it carefully. At first check what exactly is being asked?

Is it asking you to file a return? Or submit investment proofs? Maybe all you need to do is just explain a specific bank transaction? The notice is specific by law. In other words, it must tell you exactly what it needs.

Step 2: Gather Your Documents

Depending on what the AO has asked, collect:

- Bank statements for the relevant financial year

- Proof of any deductions claimed (80C investments, medical insurance, etc.)

- Capital gains statements from brokers or mutual fund houses

- Invoices or payment proofs for freelance or business income

Step 3: Log In To The E-Filing Portal

Go to incometax.gov.in. Log in with your PAN. Under “Pending Actions,” click “e-Proceedings.” After that, you will find the notice listed there. All responses are submitted digitally.

However, the best part is that the entire process is faceless. To clarify, there are no in-person meetings or officer visits.

Step 4: Submit Before The Deadline

Upload your documents with a written explanation. Keep your response factual and clear.

If you need more time, you can request an extension through the portal itself. For clarification, most AOs grant it for genuine reasons, such as a pending Form 16 or medical issues.

If the AO is satisfied, the proceedings close. If not, they may ask follow-up questions. And the same process again.

Pros And Cons Of Responding Promptly

Responding to this notice on time is not really optional, but here’s how early action compares to delay:

Pros Of Responding Promptly:

- Proceedings close quickly, often within weeks

- Avoids all penalties and escalation

- Builds a clean tax compliance record

- Gives you a chance to correct genuine errors before the assessment is finalized

Cons Of Ignoring Or Delaying:

- Penalty of ₹10,000 per instance under Section 271(1)(b)

- Risk of a Best Judgment Assessment, where the AO calculates your tax without your input

- Possible prosecution with jail time of up to one year under Section 276D

- Increased future scrutiny of your returns

What Happens If You Don’t Respond To The Section 142(1) Income Tax Notice

This is where it gets serious. Ignoring the notice is the single biggest mistake taxpayers make.

| Consequence | Details |

|---|---|

| Penalty under Section 271(1)(b) | ₹10,000 for each instance of non-compliance |

| Best Judgment Assessment under Section 144 | AO calculates your tax without your input — almost always results in a higher demand |

| Prosecution under Section 276D | Up to 1 year imprisonment, with or without a fine |

| Search warrant under Section 132 | In extreme cases, authorities may issue one |

| Higher future scrutiny | Your returns may be flagged in subsequent years |

The Best Judgment Assessment is the one to genuinely fear. When the AO doesn’t have your documents, they look at your bank credits, property records, reported investments, and anything else available.

After that, they calculate what they think you owe. They are not required to assume the most favourable interpretation. The result is nearly always a tax demand far higher than your actual liability.

Priya responded within 12 days. She filed a revised computation, submitted her bank statements, and paid the shortfall tax plus interest. The AO closed the case. Therefore, she had to encounter no penalty and no further scrutiny.

Should Beginners Worry About This Notice?

Short answer: No, if you file correctly. Yes, if you ignore it.

If you are just starting out, filing your first or second ITR, starting a SIP, and opening a trading account, here is what you need to know. Most people who get a 142(1) notice have one of these situations:

- Skipped filing their ITR for a year

- Had a high-value transaction they didn’t explain (cash deposits, property, large investments)

- Claimed deductions without maintaining proper records

Therefore, file on time, report all income sources. For example, salary, freelance, interest, capital gains, and everything else.

At the same time, you have to keep your investment documents. That’s it. The probability of this notice drops significantly.

Common Mistakes To Avoid

- Ignoring the notice. It doesn’t go away. It escalates into a Best Judgment Assessment with higher demands.

- Assuming it’s a scam. Always verify by checking your e-filing account at incometax.gov.in. Scam notices only arrive by email with suspicious links. Real notices appear in your account.

- Filing the wrong ITR form. If you have income from capital gains, rental property, or multiple sources, you may need ITR 2 instead of ITR 1.

- Filing the wrong form creates gaps that invite future notices. This is one of the most common errors among new investors.

- Not keeping investment records. Starting a SIP or a trading account? Save your annual statements.

- These may be needed the moment a notice lands.

Section 142(1) VS. Other Notices: The Key Differences

People often confuse this with other income tax notices. Here’s a simple breakdown:

- Section 143(1): An intimation, not a notice. Most importantly, 143(1) confirms that your return was processed. May show a small mismatch in tax calculations.

- Section 142(1): An inquiry notice. The AO needs more information before completing your assessment.

- Section 143(2): A scrutiny notice. Means your return has been selected for detailed examination. More serious than 142(1).

- Section 148: A reopening notice. Means the AO believes income from a prior year was not fully declared.

Among all of these, 142(1) is the most routine, and the easiest to resolve if you respond on time. Even tax professionals generally regard income tax notice section 142(1) as a procedural checkpoint rather than a punitive action.

A Simple Framework For Handling Any Tax Notice

Step 1: Log into incometax.gov.in. Check “e-Proceedings” under “Pending Actions.”

Step 2: Read what is being asked. Accordingly, file a return, submit documents, or explain a transaction.

Step 3: Collect all relevant financial records for the assessment year mentioned.

Step 4: Draft a clear, factual response. Attach documents. If the language feels complex, a CA can help for that specific task. You don’t need to hand over your entire tax life.

Step 5: Submit through the portal before the deadline. Save the acknowledgement number.

Step 6: Wait for the AO’s reply. If satisfied, proceedings close. If follow-up questions arrive, respond the same way.

Solving Common Queries And Confusions Of Tax Filers

If you want a quick answer, here’s answering the most common queries that people place on the internet regarding section 142(1) income tax notice:

Can A Section 142(1) Notice Be Issued Even If I Already Filed My Return?

Yes. Filing your ITR doesn’t automatically close the matter. If the AO finds discrepancies or needs supporting documents after you file, they can still send this notice. Filing is step one. Responding to questions is step two.

Is There A Time Limit For Issuing This Notice?

There is no fixed outer time limit in the law. The notice can be issued even after the relevant assessment year ends. However, in standard cases, the AO generally cannot demand documents more than 3 years old.

What If I Don’t Agree With What The Notice Is Asking?

You have the right to seek clarification. Legal precedents have established that a 142(1) notice must be specific. A vague or blanket request can be challenged. Mention the objection politely in your written response.

Can I Respond Myself, Or Do I Need A CA?

For straightforward cases, like submitting bank statements or confirming a known transaction, most people can respond on their own. If undisclosed income, large investment discrepancies, or business accounts are involved, a CA is worth the cost.

What Is A Faceless Assessment?

Since 2020, most income tax proceedings in India have been completely digital. You submit documents online, and a team reviews your case remotely. There is no physical interaction with any AO. This reduces bias and significantly speeds up resolution.

Will This Notice Show Up On My Credit Report?

No. Income tax proceedings do not directly affect your CIBIL score. However, a large unpaid tax demand could affect your broader financial health, which lenders may assess through other means.

What If I Need More Time To Respond?

Request an extension through the e-Proceedings portal. Mention a specific reason, which can be pending Form 16, travel, medical issues, or awaiting documents from your employer. Extensions are granted in most genuine cases.

Caution: The best protection against this Section 142(1) income tax notice is boring but true: file your ITR on time, report every source of income, and keep your documents. And if the notice does arrive, now you know exactly what to do.

Information Last Updated on Govt. Portal: June 2025. Information is based on the Income Tax Act, 1961 and CBDT guidelines applicable for AY 2025-26.

Share this article: