- Why Most Small Businesses Get Blindsided By The Portal

- The Core Characteristics Of GST Deadlines

- The Complete Return Breakdown: GSTR-1 VS. GSTR-3B VS. Annual Returns

- Master Compliance Calendar For FY 2025-26

- Pros and Cons Of Going Quarterly (The QRMP Scheme)

- The Benefits

- The Risks

- What Beginners Misunderstand About The GSTR-2B Credit System

- The True Cost of Delay: Math vs. Myths

- A Concrete Penalty Comparison

- The Ultimate Decision: Should You File Monthly or Use QRMP?

- Choose the QRMP Scheme If:

- FinanceTeam’s 4-Step Bulletproof Compliance Framework

- Reality Check: The Portal's Date Beats Online Guides

- What Changed Recently? (Critical 2026 Portal Updates)

- Common Beginner Pitfalls

- The "Nil Return" Oversight

- The Input Credit Mismatch

- How a Professional Financial Advisor Helps You Navigate Compliance

- Frequently Asked Questions

GST Filing Last Date 2026: The Secret Cost Of Missing Your Deadline By 24 Hours

GST filing last date is the final calendar day set by Indian tax authorities for a business to submit its tax returns without incurring penalties. It involves reporting sales, purchases, and tax collected under the Goods and Services Tax system.

It offers a structured way to maintain legal compliance but comes with the risk of daily late fees, heavy interest charges, and blocked tax credits if missed by even a single day.

Why Most Small Businesses Get Blindsided By The Portal

Most online guides show you a clean table of dates and call it a day. If you are running a business for the first time, you quickly learn that the calendar is not your biggest problem. The real issue is that nobody tells you what happens 30 minutes after you hit a deadline.

You do not just face a small fine from the government. You risk ruining your relationships with your biggest clients.

Let us look at a real scenario that plays out across India every month. Imagine a graphic designer named Kabir who lives in Mumbai.

He recently registered for GST because his corporate clients demanded it. He finished a major branding project for a corporate client in June.

He sent an invoice for ₹1,00,000 plus 18% GST. The client paid the full ₹1,18,000 on time.

Kabir knew his monthly tax summary return was due on the 20th of July. He had the money set aside. He planned to log in on the weekend and finish everything.

However, he forgot that his sales details had to be uploaded in a separate form by the 11th of July.

On the 15th of July, he received an angry phone call from the client’s finance manager. The client could not see the tax credit in their portal. Why?

Because Kabir missed the earlier deadline. His client’s money was locked up, and suddenly Kabir looked unprofessional.

This article will change how you look at tax compliance. We will look at what other portals ignore.

We will break down exactly:

- how missing a deadline impacts your cash flow

- how to handle unexpected portal crashes,

- and how these rules connect to everyday things like

- your restaurant GST rate bills or business insurance setups.

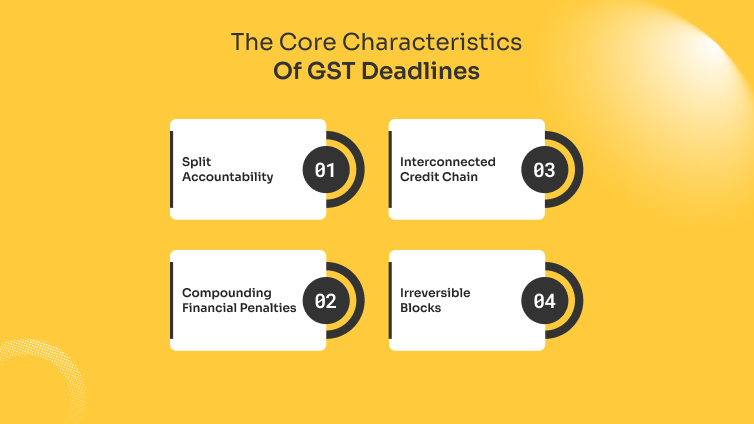

The Core Characteristics Of GST Deadlines

Before you map out your month, you need to understand how the system behaves. The Indian tax portal does not work like a traditional corporate filing system. It has specific, unyielding features:

- Split Accountability: You cannot report what you sold and pay your taxes in a single step. The system forces you to declare sales first so buyers get their credits, then calculate your final tax payment later.

- Compounding Financial Penalties: The moment the clock strikes midnight on the due date, the system automatically calculates a daily fine. You cannot negotiate this fee away.

- Interconnected Credit Chain: Your deadline is directly tied to your customer’s bank account. If your filing is late, their tax discount is delayed.

- Irreversible Blocks: If you ignore your monthly filings for more than three years, the portal permanently locks that tax period. You lose the right to file it entirely.

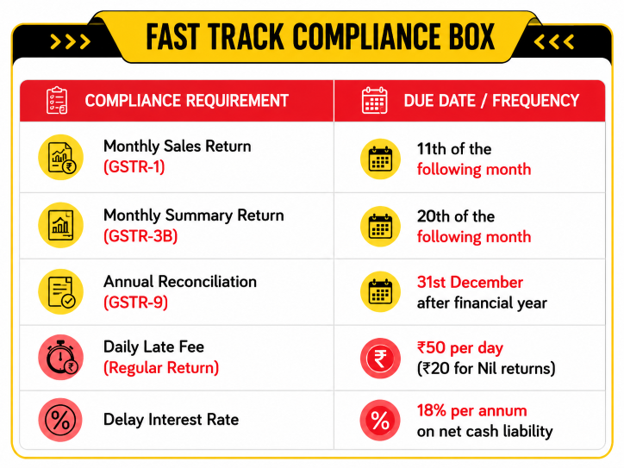

The Complete Return Breakdown: GSTR-1 VS. GSTR-3B VS. Annual Returns

Choosing the wrong filing frequency or confusing your forms can drain your business capital. The table below outlines every major return you will encounter in 2026.

Master Compliance Calendar For FY 2025-26

| Return Type | What It Reports | Who Must File It | Standard Due Date | Filing Frequency |

| GSTR-1 | Itemized sales and outward supplies | All regular registered taxpayers | 11th of the next month (13th after quarter for QRMP) | Monthly or Quarterly |

| GSTR-3B | Summary of tax liability, credits claimed, and payment | All regular registered taxpayers | 20th of the next month (22nd or 24th for QRMP) | Monthly or Quarterly |

| CMP-08 | Quarterly challan for tax payment | Composition scheme dealers | 18th of the month following the quarter | Quarterly |

| GSTR-4 | Simplified annual summary | Composition scheme dealers | 30th April after the financial year ends | Annual |

| GSTR-9 | Final annual reconciliation | Taxpayers with turnover above ₹2 Crore | 31st December after the financial year ends | Annual |

| GSTR-9C | Self-certified reconciliation statement | Taxpayers with turnover above ₹5 Crore | 31st December after the financial year ends | Annual |

Pros and Cons Of Going Quarterly (The QRMP Scheme)

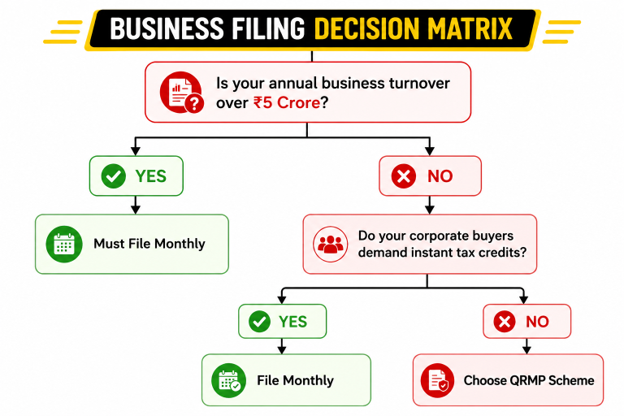

If your annual aggregate turnover is under ₹5 Crore, the government gives you a choice. You can file every month, or you can opt for the Quarterly Return, Monthly Payment (QRMP) scheme. It sounds like an easy decision, but it has hidden trade-offs.

The Benefits

- Fewer Portal Sessions: Instead of filing 24 major returns per year, you file only 8. This saves hours of administrative work or cuts down your monthly accounting bills.

- Predictable Cash Flow: You still calculate and deposit your tax every month using a simple system called Form PMT-06, but you do not have to do a full ledger reconciliation until the quarter ends.

- Fewer Late Fee Triggers: Since the actual return deadlines happen only four times a year, your chances of accidentally triggering a daily late fee drop significantly.

The Risks

- Unhappy Corporate Buyers: If you sell to large businesses, they want to see their tax credits instantly. Under QRMP, your invoices only appear every three months unless you use an optional tool called the Invoice Furnishing Facility (IFF) between the 1st and 13th of the month.

- Delayed Error Correction: If you make a typo on an invoice in January, you might not catch it or fix it until April. By then, the error could have impacted your buyer’s monthly cash balances.

- Complex Eligibility Window: You cannot jump in and out of the scheme at will. You can only switch during the first month of a quarter, which requires careful planning.

What Beginners Misunderstand About The GSTR-2B Credit System

The biggest myth among new business owners is simple: “If I paid GST to my suppliers, I can automatically deduct it from the taxes I owe the government.”

In reality, the government does not care about your paper receipts or bank statements when you calculate your monthly bill. You can only claim a tax deduction if that specific purchase appears inside your auto-generated GSTR-2B statement.

This statement freezes on the 14th of every month. It gathers data from every single one of your suppliers. If your supplier forgets to file their returns by their own GST filing last date, their invoice will not appear in your portal.

Let us say you bought new laptops for your office. The store charged you ₹50,000 plus ₹9,000 GST. If that store files their paperwork late, your portal will show zero credit on the 14th.

When you file your own taxes on the 20th, you must pay your full tax liability out of your own pocket. You have to wait until the following month to claim the ₹9,000 refund. For a startup, this sudden cash drain can cause serious problems.

The exact same thing happens with your business expenses. For example, when you review your corporate insurance policies, the gst on insurance premium can be as high as 18%.

If your insurance provider does not upload your company’s GST number correctly before their monthly deadline, that large tax credit gets locked up for weeks.

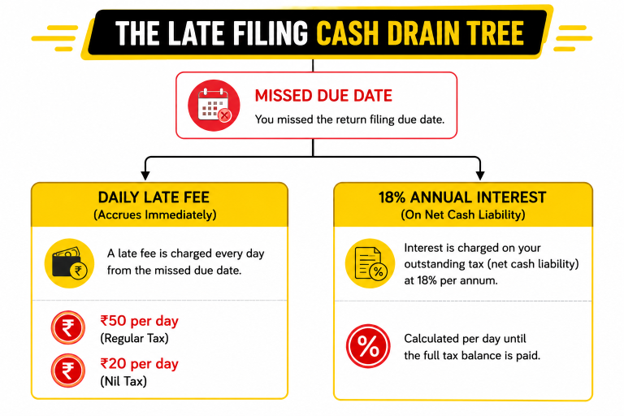

The True Cost of Delay: Math vs. Myths

Many people assume that missing a deadline by 48 hours is no big deal. They think they can just pay a small fine later. Let us break down how the numbers actually add up.

The Late Fee: For a regular return with tax due, the fee is ₹50 per day (₹25 for Central GST and ₹25 for State GST).

- Even if you had absolutely zero sales during the month, a late “Nil” return still triggers a fee of ₹20 per day. These fees accumulate automatically until they hit statutory caps.

- The Interest Charge: You must pay an annual interest rate of 18% on the tax amount you owe.

- Crucially, this interest is calculated only on your Net Cash Liability. This means you pay interest on the portion of the tax you pay through your bank account, not the portion covered by your existing tax credits.

A Concrete Penalty Comparison

Let us look at two different business owners who missed their GSTR-3B deadline by exactly 14 days. Both owed ₹1,00,000 in gross tax for the month.

- Taxpayer A (Retail Shop): They had ₹80,000 available in valid tax credits from their wholesale purchases. They needed to pay the remaining ₹20,000 in cash.

- Taxpayer B (Service Provider): They had zero tax credits available. They had to pay the entire ₹1,00,000 in cash.

| Penalty Component | Taxpayer A (Low Cash Liability) | Taxpayer B (High Cash Liability) |

| Gross Tax Due | ₹1,00,000 | ₹1,00,000 |

| Credit Deducted | ₹80,000 | ₹0 |

| Net Cash Paid | ₹20,000 | ₹1,00,000 |

| Days Delayed | 14 Days | 14 Days |

| Fixed Late Fee (14 days × ₹50) | ₹700 | ₹700 |

| Interest Formula | (₹20,000 × 18% × 14/365) | (₹1,00,000 × 18% × 14/365) |

| Interest Charged | ₹138 | ₹690 |

| Total Penalty Paid | ₹838 | ₹1,390 |

Notice how Taxpayer B pays nearly double the total penalty simply because they could not offset their tax using verified portal credits.

The Ultimate Decision: Should You File Monthly or Use QRMP?

Choose Monthly Filing If:

- You primarily sell to other registered businesses (B2B). They will constantly monitor their portals to ensure your sales invoices appear before the 14th of the month.

- Your monthly business expenses are high, and you need to use your tax credits immediately to keep your bank balances healthy.

- You prefer to close your accounting books every 30 days so you do not have to manage a massive backlog of invoices at the end of the quarter.

Choose the QRMP Scheme If:

- You sell directly to everyday consumers (B2C), such as running a local retail store or a direct-to-consumer website. These buyers do not claim business tax deductions, so they do not check the portal for your invoices.

- You run a small operation with very few monthly transactions and want to minimize your monthly paperwork and accountant fees.

- You have a disciplined cash flow system that allows you to calculate and deposit your estimated tax payments by the 25th of every single month using a challan.

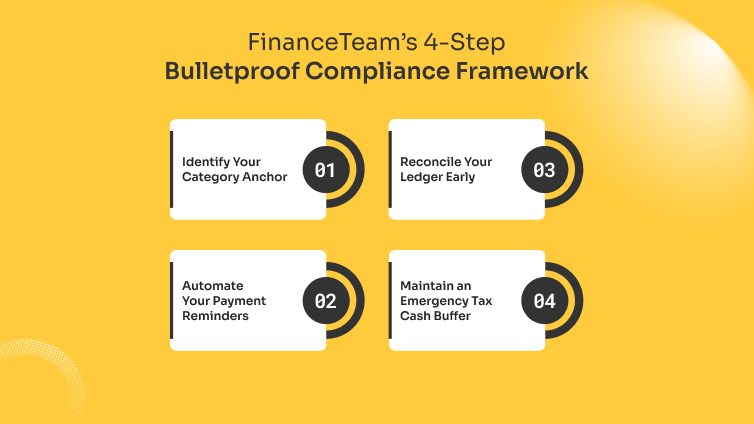

FinanceTeam’s 4-Step Bulletproof Compliance Framework

Instead of constantly stressing over dates or waiting for your accountant to call, use this simple framework to protect your business.

- Step 1: Identify Your Category Anchor: Look at your previous year’s total sales. If it is under ₹5 Crore, deliberately choose your filing track on the portal during the first month of the financial year. Do not let the portal select a default option for you.

- Step 2: Automate Your Payment Reminders: Set up recurring phone alerts for the 9th and the 18th of every month. This gives you a clear 48-hour buffer before the official GSTR-1 and GSTR-3B deadlines hit, leaving plenty of room to handle documentation issues.

- Step 3: Reconcile Your Ledger Early: Never wait until the 20th to check your tax credit balance. Log into the portal on the 15th of the month. Download your fresh GSTR-2B statement and instantly identify any suppliers who forgot to upload their invoices.

- Step 4: Maintain an Emergency Tax Cash Buffer: Always set aside the tax portion of every payment you receive into a separate business savings account. Treat that money as if it belongs to the government from day one. This ensures you never have to delay a filing due to a temporary cash shortage.

Reality Check: The Portal’s Date Beats Online Guides

Here is an honest truth about running a business: online compliance calendars can be outdated. The government frequently adjusts filing timelines through sudden official announcements.

These deadline extensions are often highly specific. They might apply only to a particular return type, a single state facing severe weather, or businesses using specific billing methods.

For instance, if your business expands and crosses the ₹10 Crore sales mark, you must comply with strict e invoice rules. Every sale must have an official digital registration number before it can legally appear on your GSTR-1 form. If your electronic billing system crashes on the 10th of the month, your standard deadline does not automatically change.

Similarly, if you run a local food joint, the restaurant gst rate you charge determines your monthly tax collection layout. A portal change affecting food delivery platforms might shift how your specific transactions are recorded, even if the general filing calendar looks exactly the same for a retail shop next door.

Always treat third-party calendars as general planning tools. The official dashboard on the GST portal is the only single source of truth for your specific account.

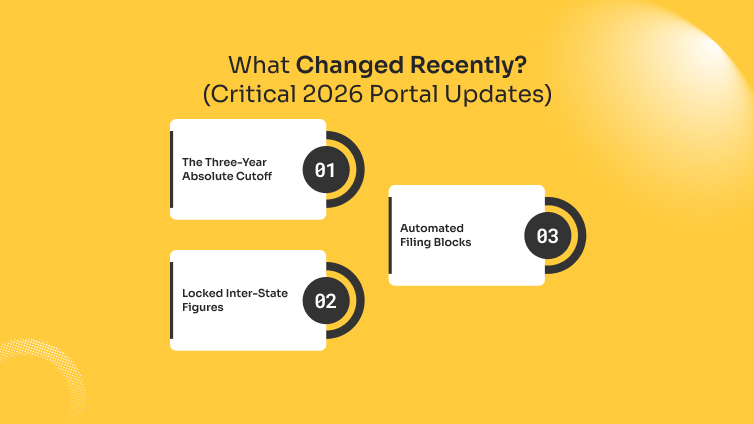

What Changed Recently? (Critical 2026 Portal Updates)

The rules governing the tax portal have become far stricter. If you are catching up on old business filings, you need to be aware of these recent updates:

- The Three-Year Absolute Cutoff: You can no longer submit a GSTR-3B return if it is more than three years past its original due date. Once that window closes, that tax period is permanently blocked.

- Locked Inter-State Figures: The portal now auto-populates all inter-state sales figures directly from your GSTR-1 into your GSTR-3B. You can no longer manually edit these numbers during the final payment step. If you made an error, you must use a correction form called GSTR-1A before your final filing.

- Automated Filing Blocks: If you forget to file your GSTR-1 sales details for a month, the system will block you from submitting your GSTR-3B return for that period. You can no longer skip steps to save time.

Common Beginner Pitfalls

When you handle your taxes for the first time, it is easy to make simple mistakes that become expensive lessons.

The “Nil Return” Oversight

Many entrepreneurs believe that if their business made zero sales in a month, they do not need to take any action. This is a costly mistake. You must log in and submit a “Nil” return. If you do not, the system will add a ₹20 fine to your account every single day until you comply.

The Input Credit Mismatch

Never guess your input tax deduction numbers or input them based on your paper purchase receipts. If the number you type into your GSTR-3B return is higher than the amount shown in your official GSTR-2B statement, the portal will flag your account. You will receive an automated system notice demanding you pay back the difference with interest.

How a Professional Financial Advisor Helps You Navigate Compliance

When you launch a business, it is easy to get overwhelmed by these moving parts. It might feel like you need to become a tax lawyer just to keep your business running smoothly. This is exactly where a qualified financial advisor or an experienced chartered accountant steps in.

A good advisor does not just fill out forms and tell you what you owe at the end of the month. Their real job is to take these complicated, stressful tax systems and turn them into simple, predictable business routines.

They look ahead at your business operations. They help you choose between monthly or quarterly filings based on your true cash requirements. They make sure you never miss out on valuable tax deductions from large expenditures like insurance setups or equipment purchases.

By handling the operational relationship with the portal, a professional protects your credit score, keeps your corporate clients happy, and frees up your time so you can focus entirely on growing your business.

Frequently Asked Questions

If a major technical glitch causes widespread portal crashes, the government usually issues an official notification extending the gst filing last date by a day or two.

However, small local network issues or computer crashes do not excuse you from penalties. It is always safest to file your returns at least three days before the final deadline to avoid last-minute portal slowdowns.

You cannot directly edit or overwrite a GSTR-1 or GSTR-3B return once it is successfully submitted. Instead, you must enter any corrections, missing invoices, or credit adjustments into the corresponding fields of the return you file in the following month.

Log into your account on the official portal, navigate to the ‘Search Taxpayer’ section, and enter your supplier’s unique GST identification number. The system will display their complete filing history, showing you exactly which months they completed on time and which ones are still pending.

No. The annual GSTR-9 reconciliation return is completely optional for businesses whose aggregate annual turnover is under ₹2 Crore.

If your turnover stays below this threshold, your monthly or quarterly filings are considered sufficient for the financial year.

The government sets maximum caps on late fees to protect small businesses from infinite penalty growth.

For businesses with zero sales activity, the total fee is capped at ₹500 per return. For small businesses with an annual turnover under ₹1.5 Crore, the maximum penalty is capped at ₹2,000 per delayed return.

Share this article: