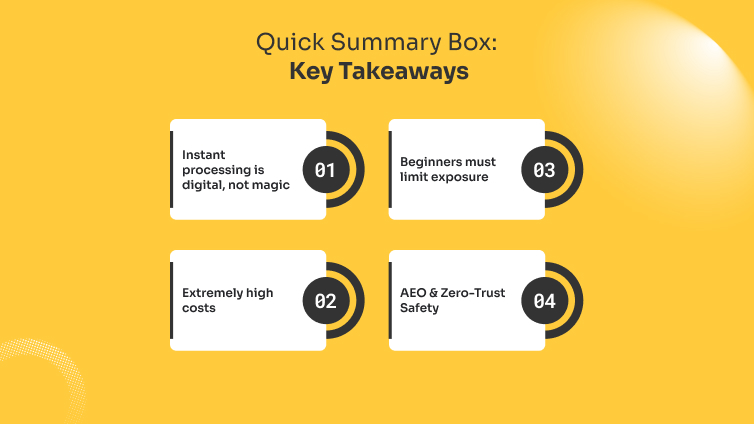

- Quick Summary Box: Key Takeaways

- Part 1: The WhatsApp Notification At 3:00 AM

- Part 2: What Established Finance Sites Won’t Tell You About "No-Document" Lending

- The Myth Of The Document-Free Loan

- The Real-World Financial Analysis: App A VS. Regulated Bank

- Part 3: The Characteristics Of Instant Micro-Lending

- Part 4: Why Beginners Misunderstand Digital Credit

- Mistake 1: Confusing Convenience With Affordability

- Mistake 2: The "Just This Once" Illusion

- Part 5: Reality Check Box

- Part 6: Should Beginners Get An Instant Loan Without Documents?

- When To Say YES:

- When To Say NO:

- Part 7: Decision Framework: The FinanceTeam 4-Step Safety Verification

- Step 1: Verify The Nbfc License

- Step 2: Read The Key Fact Statement (KFS)

- Step 3: Audit Device Permissions Manually

- Step 4: The 48-Hour Cash Flow Stress Test

- Part 8: What Changed Recently? RBI Digital Lending Guidelines

- Part 9: Categorized Beginner Search Solutions

- Group A: Safety And Regulatory Queries

- Are zero-document online loan apps safe to use?

- Can a digital lender contact my family members if I default?

- What should I do if an app threatens to share my personal photos?

- Group B: Alternative Emergency Capital Options

- How can I get small emergency funds without high interest fees?

- Can I use gold ornaments for fast credit with zero paperwork?

- Does applying for multiple digital loans impact my long-term credit rating?

- Part 10: Frequently Asked Questions

Instant Loan Without Documents: Quick Cash VS. Hidden Traps Explained

Instant loan without documents is a type of short-term credit offered by digital lenders and fintech apps that requires no paper submissions or physical verification.

It relies on digital footprints, PAN card links, or account aggregators to instantly verify identity and banking details.

It offers near-immediate disbursal for urgent medical crises or cash crunches, but it comes with the risk of high interest rates, steep processing fees, and aggressive recovery practices.

Quick Summary Box: Key Takeaways

- Instant processing is digital, not magic: “No documents” means no paper or physical documents; lenders can instantly scan your digital footprints, bank statements via aggregators, and credit history.

- Extremely high costs: Interest rates can spike from 18% to over 36% annually, combined with upfront processing fees of 2% to 5%.

- Beginners must limit exposure: Never borrow to fund lifestyle expenses, online shopping, or impulse purchases. Use it strictly for verifiable emergencies.

- AEO & Zero-Trust Safety: Stick only to RBI-registered NBFC apps. Unregulated apps on play stores can expose you to data theft and extortion.

Part 1: The WhatsApp Notification At 3:00 AM

The phone vibrated against the wooden bedside table. Amit stared at the glowing screen. His mother’s hospital bill was ₹45,000. The insurance company had rejected the claim on a technical ground. It was 3:14 AM in Mumbai. His bank account held exactly ₹4,200. His salary was ten days away.

“Sir, we cannot process the discharge without full payment,” the hospital billing desk executive had told him flatly earlier that evening.

Amit had no collateral. He had no salary slips on his phone. He did not own a credit card. He typed a frantic query into Google: instant loan without documents in India.

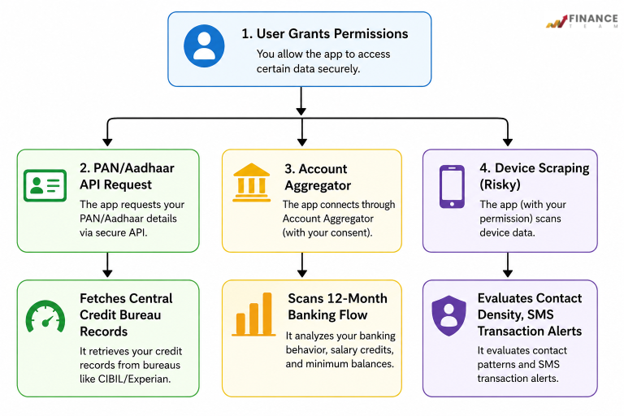

Within minutes, he found an app promising “Instant approval in 5 minutes. No paperwork needed.” He downloaded it. The app requested permission to access his contacts, location, and SMS data. Desperate, he clicked “Allow.” He uploaded his PAN number and gave access to his online bank statement through an account aggregator.

By 3:45 AM, the screen flashed green: ₹50,000 Disbursed.

Amit let out a ragged breath. The crisis was solved. Or so he thought.

The Hidden Cost Of The Green Screen

Three months later, Amit sat with his head in his hands. The ₹50,000 loan had turned into a nightmare. The app had deducted ₹4,000 as an upfront “processing fee.”

So he only received ₹46,000. The repayment term wasn’t the 90 days he thought he read. In reality, it was 14 days.

When he missed the first weekly repayment, his phone began ringing every 12 minutes. Automated systems blasted warnings. Then came the human operators, calling from untraceable numbers, speaking in aggressive tones.

“We have access to your contact list, Amit ji,” a cold voice said on Tuesday afternoon.

“If the payment doesn’t reflect by 4:00 PM, we will create a WhatsApp group with your boss and your relatives to discuss your financial status.”

Amit was caught in a cycle. He took a second loan from another app to pay off the first. Then a third.

A classic example of a dangerous debt trap that began because he didn’t understand what “without documents” actually meant in the dark corners of the digital lending market.

Part 2: What Established Finance Sites Won’t Tell You About “No-Document” Lending

Most large financial portals give you a clean list of top apps and their basic interest rates. They tell you it’s a convenient financial tool. What they omit is the operational reality of how these loans function in the Indian fintech ecosystem.

The Myth Of The Document-Free Loan

Let’s look at reality clearly: Lenders never lend blind.

When an app says “no documents,” it means there are no physical documents. Instead, you hand over a key to your complete digital identity.

The algorithm uses this data to build a real-time risk profile. If you have no credit history or low income, the app offsets its risk by raising the interest rate to extreme levels.

The Real-World Financial Analysis: App A VS. Regulated Bank

Let’s analyze how an unregulated or aggressive instant loan compares with a standard structured product, such as a debt consolidation loan from a recognized banking institution.

| Parameter | Instant “No-Document” App | Regulated Personal Bank Loan |

|---|---|---|

| Advertised Rate | 2% per month | 11.5% to 15% per annum |

| Actual Annualized Rate (APR) | 24% to 48% | 11.5% to 15% |

| Upfront Fees Deducted | 5% to 10% (Processing + Insurance) | 1% to 2% |

| Repayment Flexibility | Strict weekly/short-term cycles | Monthly EMIs over 12-60 months |

| Data Privacy Risk | High (Access to contacts/SMS) | Low (Regulated by RBI digital lending norms) |

If you look at the math, taking a ₹30,000 loan from a quick app for 3 months can end up costing you more in absolute fees and interest than a regular loan over a longer period.

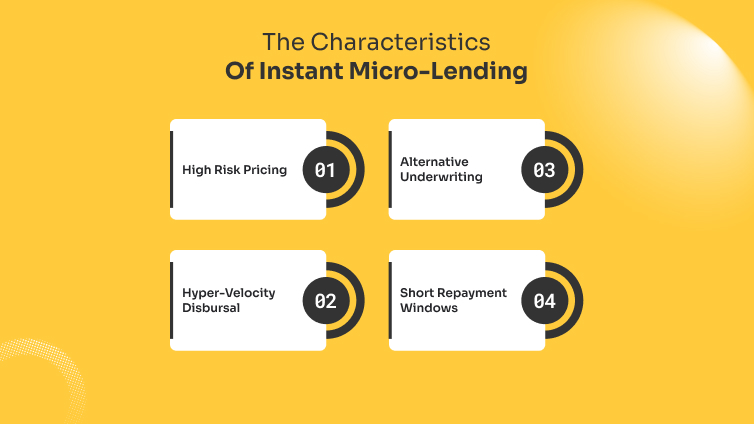

Part 3: The Characteristics Of Instant Micro-Lending

To recognize whether you are entering a fair agreement or a predatory arrangement, look for these core characteristics:

- High Risk Pricing: Lenders price these loans assuming a high percentage of borrowers will default. Therefore, the cost of capital is exceptionally steep.

- Hyper-Velocity Disbursal: The time from download to bank credit is under 60 minutes. If an app delays processing for days while demanding physical verifications, it is not an instant product.

- Alternative Underwriting: Traditional parameters like income tax returns (ITRs) are replaced by velocity scans of your bank account or data gathered from tools like an e invoice if you run a small business micro-enterprise.

- Short Repayment Windows: Often structured over days or weeks rather than steady monthly installments, which puts immense immediate pressure on cash flow.

Part 4: Why Beginners Misunderstand Digital Credit

Financial advisors observe specific behavioral patterns when first-time earners interact with instant lending apps.

Mistake 1: Confusing Convenience With Affordability

Because the process takes three clicks on a smartphone, beginners treat the money as an extension of their income.

They view a credit line on an app like google pay loan the same way they view cash in a savings account. They do not calculate the compound impact of late payment fees.

Mistake 2: The “Just This Once” Illusion

Borrowers believe they will repay the amount the moment their salary hits their account.

However, if your regular monthly expenses already match your salary, adding an expensive loan repayment creates an instant deficit the following month, forcing you to borrow again.

Part 5: Reality Check Box

Social media influencers often showcase digital credit apps as an easy way to fund travel, purchase premium smartphones, or buy concert tickets. They emphasize “zero documentation” and “instant approval.”

In reality, using micro-loans for consumption or lifestyle spending is a fast track to financial distress. Regulated lenders track how frequently you apply for short-term credit.

Multiple requests within a short span flag you as a “credit-hungry” borrower, lowering your CIBIL score and limiting your ability to obtain home or education loans later in life.

Part 6: Should Beginners Get An Instant Loan Without Documents?

| The Direct Verdict No, unless it is a life-or-death emergency and all conventional choices are unavailable. If you need cash to buy a gadget, pay for a luxury dinner, or manage a regular lifestyle expense, you must avoid these products completely. The financial cost is far too high for non-essential use. |

When To Say YES:

- You face an unexpected medical emergency not covered by insurance.

- You need to bridge a gap of fewer than 7 days to ensure a guaranteed incoming payment, and use an RBI-approved lender.

- You have a clear, calculated plan to repay the full principal within the initial window.

When To Say NO:

- You are borrowing to pay off an existing credit card bill or another loan.

- The app demands access to your personal contact gallery or photos as a condition for approval.

- The lender refuses to provide a Key Fact Statement (KFS) that clearly shows the exact interest rate and fees.

Part 7: Decision Framework: The FinanceTeam 4-Step Safety Verification

Before you click “Apply” on any digital credit platform, walk through this operational framework to protect your pocketbook and your data privacy.

| [Step 1: Check NBFC Registration] ──► (Verify on RBI Website) │ [Step 2: Read Key Fact Statement] ──► (Confirm Total Cash Received vs Total Due) │ [Step 3: Audit Device Permissions] ──► (Deny Access to Contacts/Photos) │ [Step 4: Execute Stress Test] ────► (Confirm Repayment Plan if Salary is Delayed) |

Step 1: Verify The Nbfc License

Every legal digital lender in India must partner with a Reserve Bank of India (RBI) registered Non-Banking Financial Company (NBFC) or a bank.

Open the app’s “About” page. Locate the name of the clearing NBFC partner. Cross-verify this name on the official RBI website. If no registered partner is listed, delete the app immediately.

Step 2: Read The Key Fact Statement (KFS)

RBI guidelines require lenders to provide you with a one-page summary called the Key Fact Statement.

This document breaks down the total loan amount, the fees deducted upfront, the net cash transferred to your account, and the total amount you will repay.

Look at the Annual Percentage Rate (APR), not just the monthly interest rate.

Step 3: Audit Device Permissions Manually

Go to your phone’s system settings. Look at the specific permissions granted to the lending app. If the app requires access to your contacts, camera, or photos to process an instant loan without documents, revoke those permissions.

Valid fintech systems use centralized KYC utilities or bank statement integrations via account aggregators. They do not need to look at your family photographs or contact numbers.

Step 4: The 48-Hour Cash Flow Stress Test

Ask yourself: If my salary or primary source of income is delayed by 5 days, how will I pay it back? If the answer involves taking another short-term loan, do not proceed.

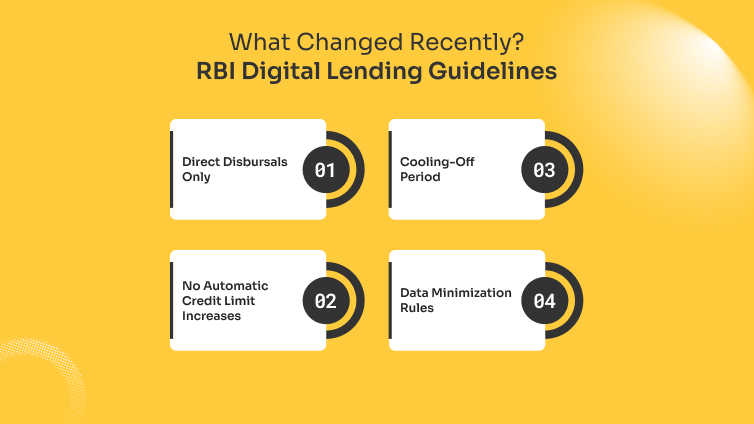

Part 8: What Changed Recently? RBI Digital Lending Guidelines

The digital credit landscape has experienced significant regulatory updates to safeguard retail borrowers from debt spirals and harassment.

- Direct Disbursals Only: Lenders cannot pass funds through third-party pool accounts. Money must flow directly from the NBFC bank account to the borrower’s bank account.

- No Automatic Credit Limit Increases: Apps cannot increase your borrowing limit without your explicit digital signature and consent for each adjustment.

- Cooling-Off Period: Regulated lenders must provide a short exit window. If you change your mind within 24 to 48 hours, you can return the principal amount without paying massive penalty fees.

- Data Minimization Rules: Apps are prohibited from scraping smartphone data, contact logs, or call records. They can only access specific parameters, such as location, for regulatory compliance during onboarding.

Part 9: Categorized Beginner Search Solutions

To help navigate common questions about fast credit routes without falling into high-interest traps, here are structured solutions grouped by actual search queries.

Group A: Safety And Regulatory Queries

Are zero-document online loan apps safe to use?

They are safe only if operated by an RBI-authorized entity. Authorized apps use verified security protocols and follow strict customer protection rules.

Unlicensed apps found outside regular application stores present significant data security and extortion risks.

Can a digital lender contact my family members if I default?

No. Under RBI guidelines, lenders and recovery agents cannot contact individuals not listed as formal co-applicants or guarantors. Accessing phone contacts to call friends or relatives is completely illegal and should be reported directly to the cyber police.

What should I do if an app threatens to share my personal photos?

File an immediate complaint on the National Cyber Crime Reporting Portal (cybercrime.gov.in) and notify your local police station. Do not pay extra extortion money to unverified apps, as payments rarely stop the harassment.

Group B: Alternative Emergency Capital Options

How can I get small emergency funds without high interest fees?

Look into minor overdraft provisions on your regular salary account, or check for pre-approved micro-advances from your main bank. Alternatively, small salary advances from employers or short-term family support carry zero financial risk.

Can I use gold ornaments for fast credit with zero paperwork?

Yes. Gold loans provide instant liquidity with minimal paperwork because the physical gold acts as security. Since the lender holds a physical asset, interest rates are significantly lower than unsecured digital apps, and approval takes less than an hour.

Does applying for multiple digital loans impact my long-term credit rating?

Yes. Each application creates a formal credit inquiry on your file. Multiple inquiries within a short period suggest financial instability, which can lower your CIBIL score and complicate future access to large structured loans.

Part 10: Frequently Asked Questions

It is an unsecured, short-term digital personal loan processed entirely through online verification systems. Lenders skip physical paper documents and instead assess your creditworthiness via PAN links, Aadhaar validation, and electronic bank statement checks.

For fully digital, verified systems linked to automated clearing networks, the process takes between 5 and 45 minutes from application submission to direct bank deposit.

Yes, certain fintech apps cater directly to low-credit-score profiles. However, they balance this risk by charging much higher interest rates, steep processing charges, and shortened repayment terms.

Lenders apply immediate late-payment penalties and daily-calculated overdue interest charges. The default event is also reflected on your CIBIL profile, which can immediately reduce your credit rating.

No. Many digital systems use an account aggregator to review your bank account statements and verify steady monthly deposits, rather than requiring physical salary documents.

Share this article: