- What Is A Debt Consolidation Loan?

- The Problem That Brings Most People Here

- See What Consolidating Your Debts Actually Saves You

- How It Actually Works

- Debt Consolidation Loan VS Personal Loan

- Recent Changes That Most Sources Don’t Cover

- These Shifts Will Be Critical If You Are Applying For A Loan In 2026

- · Your Credit Bureau Profile Matters More Than Ever

- What Does A Debt Consolidation Loan Look Like On Paper?

- What Credit Score Is Needed To Qualify For A Debt Consolidation Loan?

- Honest Pros And Cons Of Debt Consolidation Loan In India

- How A Debt Consolidation Loan Will Help You?

- Where Debt Consolidation Loan Won’t Work?

- The Biggest Misconception

- Debt Consolidation VS Loan Settlement

- Can Debt Consolidation Reduce EMI?

- Should You Actually Take A Debt Consolidation Loan?

- Check Your Debt-To-Income Ratio First

- Take A Debt Consolidation Loan If:

- Don’t Consider It If:

- Financeteam.net’s Suggestion: Follow This Step-By-Step Framework Before You Apply

- Consolidation Loan VS. The Alternatives

- Common Mistakes People Make

- What If You Have a Complaint Against a Lender?

- Best Sources To Take A Debt Consolidation Loan In India

- 1. Public & Private Sector Banks (Usually The Best Option)

- 2. NBFCs (The Flexible Middle Ground)

- 3. Balance Transfer Facilities (Often The Cheapest Option)

- 4. Fintech Lending Platforms (Use With Caution)

- 5. Loan Against Property (Best For Large Debt Consolidation)

- Comparison Table: Which Source Is Best For Debt Consolidation?

- FinanceTeam's Honest Verdict

- Key Takeaways

- FAQs

One Loan, Fewer EMIs, Same Problem? The Truth About Debt Consolidation Loan (2026 Guide)

A debt consolidation loan is a single new loan that pays off several existing debts. For instance, credit cards, personal loans, or small digital loans.

As a result, you are left with one EMI instead of many. It usually works because the new loan carries a lower interest rate than what you were paying before.

But it only helps if you stop borrowing again once it’s done. If you don’t, you can end up with the same debts, plus a new one.

That last line is the part most articles skip. And it’s the part that actually decides whether consolidation helps you or hurts you.

What Is A Debt Consolidation Loan?

A debt consolidation loan is a new loan used to combine multiple existing debts into a single repayment. Instead of managing several EMIs, credit card bills, or short-term loans, you replace them with a single loan, a single interest rate, and a single monthly payment.

The main goal is to reduce financial pressure by simplifying repayments and, ideally, lowering the overall interest cost. Debt consolidation is most effective when a large portion of your debt comes from high-interest products such as credit cards, buy-now-pay-later balances, or expensive personal loans.

- You apply for a new loan that is large enough to cover your existing debts.

- The funds are used to repay your outstanding credit cards, personal loans, or other eligible borrowings.

- Your previous debts are closed or substantially reduced.

- You begin repaying a single EMI to the new lender instead of managing multiple monthly payments.

- If the new loan carries a lower interest rate, your monthly interest burden may decrease.

- The biggest benefit comes from avoiding new debt after consolidation, allowing you to focus entirely on repaying the new loan.

In simple terms, debt consolidation doesn’t eliminate debt. It reorganizes it into a structure that may be easier and cheaper to manage.

The Problem That Brings Most People Here

You’re not Googling this out of curiosity. Rather, you’re probably juggling:

- Two or three EMIs

- A credit card bill that never seems to shrink, and

- Due dates scattered across the month like landmines

One card charges nearly 40% per year without you even realizing it. The reason is that nobody quotes credit card interest as an annual rate. To clarify, they quote it as “3.5% a month,” which sounds harmless until you do the maths.

That gap between how credit card interest is worded and what it actually costs is the entire reason debt consolidation exists as a product.

See What Consolidating Your Debts Actually Saves You

Add each debt you’re currently paying off. Then set the rate you’re being offered on a consolidation loan. After that, the tool works out the combined EMI and total interest, before and after, using the same maths a lender uses.

How It Actually Works

You take one new loan. In most cases it is usually an unsecured personal loan. Meanwhile, that loan is big enough to close out your existing debts in one go.

The lender pays off (or you pay off) the old accounts. From that point you make one EMI, to one lender, at one rate.

Here’s what that can look like in practice. Say someone is paying off ₹1,00,000 in credit card dues at 40% a year (a fairly typical card rate), alongside a ₹1,50,000 personal loan at 16%.

| Before consolidation | After consolidation | |

|---|---|---|

| Number of EMIs | 2 | 1 |

| Combined debt | ₹2,50,000 | ₹2,50,000 |

| Approx. interest rate | 40% (card) + 16% (loan), blended | ~12–13% (single new loan) |

| Monthly interest cost (rough) | Higher, because 40% is dragging up the average | Lower, single flat rate |

| Due dates to track | 2 | 1 |

(These figures are illustrative, meant to show the mechanism. Meanwhile, your actual numbers will depend on your outstanding balances, tenure, and the rate you’re offered.)

The saving comes almost entirely from replacing your highest-rate debt. That is usually the credit card, plus something cheaper.

If none of your existing debts are high-cost, consolidation won’t do much for you.

Debt Consolidation Loan VS Personal Loan

A debt consolidation loan isn’t a separate loan type. It’s a personal loan used for a specific purpose: paying off your existing debts rather than funding a purchase.

The application process, interest calculation, and eligibility rules are the same either way.

Some lenders, like Kotak Mahindra Bank and IDFC FIRST Bank, do list “debt consolidation loan” as a named product, and a few pay your old creditors directly rather than crediting your account.

But that’s a difference in labeling and disbursal, not in the underlying loan. So if you take a personal loan and use it to clear three other debts, you’ve consolidated, whether or not the lender called it that.

Recent Changes That Most Sources Don’t Cover

This is the part most debt consolidation content in India never touches. Above all, it’s directly relevant if you’re applying in 2026.

Since November 2023, the RBI has treated unsecured retail credit like personal loans, credit card dues, and consolidation loans as riskier from a bank’s own capital perspective.

Again, that raises the risk weight lenders must hold against these loans.

In plain terms: it’s now more expensive for a bank to lend you an unsecured amount than it was two years ago. Again, that cost tends to be passed on through slightly stricter approvals and pricing, rather than blanket rate hikes.

These Shifts Will Be Critical If You Are Applying For A Loan In 2026

- Instant approvals with almost no paperwork are getting rarer.

Lenders are now expected to verify income, bank statements, and employment more thoroughly. Particularly for self-employed applicants and gig workers.

If you run a small GST-registered business and use e invoice records to show income, keep them handy. To clarify, they are increasingly treated as legitimate proof of income for loan underwriting, not just a tax formality.

- Rejected once? There’s a 30-day cooling-off period

After 30 days, most lenders will reassess you. To sum up, that’s what discourages applying to five lenders in a week. Moreover, banks note that this habit quietly wrecks people’s credit scores through repeated hard inquiries.

- Penal interest on late EMIs was scrapped in mid-2025.

Lenders can still charge the standard loan interest rate on overdue amounts. But the old practice of stacking extra “penal” charges on top is no longer allowed the way it once was.

None of this means consolidation has become a bad idea. It means the “apply in five minutes with no documents” version of it is fading. On the other hand, a slightly more paperwork-heavy, income-verified version is taking its place.

· Your Credit Bureau Profile Matters More Than Ever

Before approving a debt consolidation loan, lenders typically review information reported by India’s major credit bureaus, including CIBIL, Experian, and Equifax.

Your repayment history, existing loan balances, credit utilization, and recent loan enquiries all contribute to how lenders assess risk. While a higher credit score doesn’t guarantee approval, it can improve your chances of qualifying for lower interest rates and better loan terms.

What Does A Debt Consolidation Loan Look Like On Paper?

- Unsecured: no property, gold, or asset pledged

- Fixed EMI, fixed tenure (commonly 12 to 84 months, sometimes longer)

- Interest generally lands somewhere between 10% and 24% a year, depending on your credit score, income, and lender, though weaker profiles can see higher

- Faster approval than secured loans, but slower than the old “instant loan without documents” style products, for the reasons above

- Available through banks and NBFCs, and increasingly through lending apps built on top of platforms like Google Pay loan,

- which partner with a licensed bank or NBFC behind the scenes

- Always check which regulated lender is actually disbursing the loan,

- not just the app you tapped

What Credit Score Is Needed To Qualify For A Debt Consolidation Loan?

There’s no fixed national cutoff. Banks like HDFC, ICICI, SBI, and Axis generally look for a score of 700 and above, with 750+ needed for their best rates.

NBFCs such as Bajaj Finance, Tata Capital, and Muthoot Finance are often more flexible, approving applicants from around 650, though at higher rates near 18–24%.

Digital lenders like Fibe, MoneyTap, and CASHe sometimes go as low as 600, weighing bank statements and repayment patterns alongside the score.

A higher score mainly affects your interest rate, not just approval, so improving it before applying can meaningfully lower what you pay overall.

Honest Pros And Cons Of Debt Consolidation Loan In India

A debt consolidation loan is a useful financial instrument in retailer finance. However, you need to be aware of the specific pros and cons.

It will help you to be 100% sure about what you need it for and how it will impact your financial health in the short and long term.

How A Debt Consolidation Loan Will Help You?

- Cuts your blended interest rate, mainly by replacing high-cost card debt

- Turns multiple due dates into one, which reduces missed-payment risk

- Can improve your credit score over time, if paid on time

- Gives you a fixed end date, unlike a credit card, which can go on indefinitely

Where Debt Consolidation Loan Won’t Work?

- It doesn’t erase debt; it restructures it

- If your spending habits caused the debt, the same habits can create new debt on top of the consolidated loan

- Longer tenures lower your EMI but can raise the total interest you pay over time

- A weak credit profile may only qualify for a rate that isn’t meaningfully better than what you already have

The Biggest Misconception

Most people assume a debt consolidation loan is a way to “reset.” However, in reality, it isn’t. It’s a refinancing tool.

Therefore, when you use it, you’re not making the debt disappear; you’re moving it from an expensive lender to a cheaper one. The financial pressure only actually eases if two things happen together:

- The new rate is genuinely lower, and

- You close the old accounts instead of leaving the credit limit open for future use.

Meanwhile, if you skip either one, the debt consolidation loan just adds a third EMI to the pile.

Debt Consolidation VS Loan Settlement

Debt consolidation and loan settlement are often confused, but they serve very different purposes.

A debt consolidation loan helps you continue repaying your obligations under a new structure, ideally with a lower interest rate or simpler repayment schedule.

Loan settlement involves negotiating with a lender to close a debt for less than the full outstanding amount. While settlement can reduce the immediate burden, it may negatively affect your credit profile and future borrowing eligibility.

For borrowers who can still manage repayment, consolidation is generally viewed more favorably by lenders than settlement.

Can Debt Consolidation Reduce EMI?

Yes, usually. To clarify, your EMI drops when the blended interest rate falls, or the tenure stretches out. Take someone paying ₹1,00,000 on a credit card at 40% interest and ₹1,50,000 on a personal loan at 16% interest, both over 3 years.

That works out to a combined EMI of roughly ₹8,800 a month. Consolidate the same ₹2,50,000 into a single loan at 13% over the same tenure, and the EMI drops to about ₹8,400 per month.

The savings look modest month to month. But they come from cutting the 40% portion specifically.

To sum up, the more high-cost debt you’re carrying, the bigger this gap gets. If you extend the tenure further, the EMI will fall more. However, the total interest paid may rise.

Should You Actually Take A Debt Consolidation Loan?

There is no single golden rule here. You must be objective when deciding whether to take out a loan. Let’s see who should probably opt for a debt consolidation loan and who shouldn’t.

Check Your Debt-To-Income Ratio First

A debt consolidation loan can reduce financial pressure, but only if your overall borrowing remains manageable. One useful measure is your Debt-to-Income Ratio (DTI), which compares your total monthly debt obligations with your monthly income. If a large share of your income is already committed to EMIs, consolidation may simplify repayment but won’t automatically solve affordability issues.

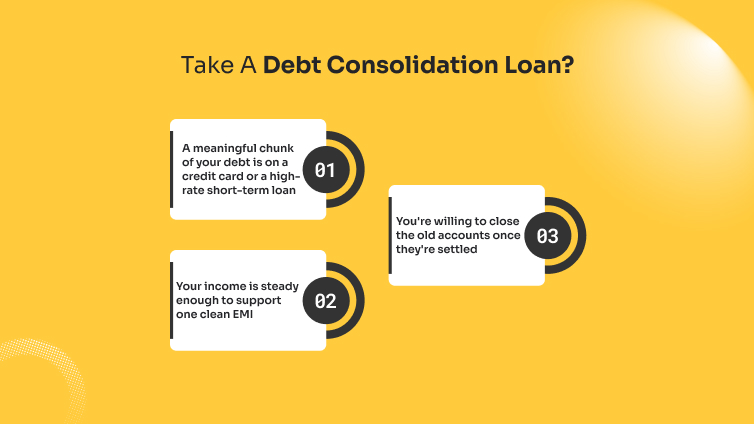

Take A Debt Consolidation Loan If:

- A meaningful chunk of your debt is on a credit card or a high-rate short-term loan

- Your income is steady enough to support one clean EMI

- You’re willing to close the old accounts once they’re settled

Don’t Consider It If:

- Your existing debts are already at reasonably low rates. In simpler words, consolidating won’t save much, and you’ll just pay processing fees for no real benefit

- Your income has recently become unstable. To clarify, a bank may reject you anyway, and the credit check itself dents your score

- You’re likely to run the credit card back up the moment it’s clear. In conclusion, it is a habit problem, not a rate problem, and a new loan won’t fix a habit

Financeteam.net’s Suggestion: Follow This Step-By-Step Framework Before You Apply

- List every debt with its actual annual rate, not the monthly number lenders quote. A monthly rate of 3–4% may translate to an annualized cost exceeding 40% once compounding is considered.

- Check your CIBIL score. Most lenders want 700+ for their better rates; below that, the consolidated rate may not beat your current blended rate.

- Get quotes from at least two or three lenders before accepting one. Remember that the rates for the same profile can differ by several percentage points between a bank and an NBFC.

- Decide what to do with the old accounts. If it’s a credit card, plan to close or freeze it after it’s paid off. An open, empty credit limit is exactly how people end up back where they started.

Consolidation Loan VS. The Alternatives

| Option | Best for | Watch out faor |

|---|---|---|

| Debt consolidation loan (bank/NBFC) | Multiple debts, at least one high-rate (like a card) | Requires income proof; approval takes a few days, not minutes |

| Balance transfer (moving existing loan to a cheaper lender) | Single loan, good repayment history | Processing fee may offset the saving on small balances |

| “Instant loan without documents” apps | Emergencies needing same-day cash | Often carries the highest effective rates of all. Minimal checks can mean minimal borrower protection too. So, read the fine print on charges before signing |

Common Mistakes People Make

- Consolidating and then keeping the old credit card active “just in case” — this is how debt doubles instead of shrinking

- Choosing the longest tenure purely to shrink the EMI, without checking the total interest that adds up over the extra years

- Applying to multiple lenders back-to-back without knowing each hard inquiry is visible to the next one

- Ignoring processing fees, which on some loans can run to 1–5% of the loan amount and quietly reduce the saving

What If You Have a Complaint Against a Lender?

If you believe a regulated bank or NBFC has treated you unfairly, charged fees incorrectly, or failed to resolve a complaint through its internal grievance process, you may be able to escalate the matter through the RBI Integrated Ombudsman Scheme.

This provides borrowers with an independent mechanism for resolving disputes involving regulated financial institutions.

Best Sources To Take A Debt Consolidation Loan In India

Not all debt consolidation loans are created equal. The best source depends on your credit score, income stability, urgency, and the type of debt you’re trying to combine.

Many borrowers focus only on the advertised interest rate, but approval odds, processing fees, repayment flexibility, and customer support matter just as much.

1. Public & Private Sector Banks (Usually The Best Option)

For most salaried borrowers with a strong credit history, banks are usually the safest and most cost-effective choice.

Real examples:

- HDFC Bank Personal Loan

- ICICI Bank Personal Loan

- SBI Personal Loan

- Axis Bank Personal Loan

- Kotak Mahindra Personal Loan

Why they work well:

- Typically offer lower interest rates than digital lending apps.

- Longer repayment tenures.

- Better customer-service infrastructure.

- Strong regulatory oversight.

Potential drawbacks:

- More documentation.

- Stricter credit score requirements.

- Slower approvals than fintech lenders.

Best for: Salaried professionals with stable income and a CIBIL score above 700.

2. NBFCs (The Flexible Middle Ground)

NBFCs often approve borrowers who don’t neatly fit traditional bank criteria.

Real examples:

- Bajaj Finance

- Tata Capital

- Aditya Birla Finance

- L&T Finance

- Piramal Finance

Why they work well:

- More flexible eligibility criteria.

- Faster approvals.

- Better suited to self-employed applicants.

Potential drawbacks:

- Interest rates can be higher than banks.

- Processing charges may be higher.

Best for: Freelancers, consultants, business owners, and borrowers with moderate credit scores.

3. Balance Transfer Facilities (Often The Cheapest Option)

If you mainly have one expensive personal loan or one large credit-card balance, a balance transfer can be smarter than taking a completely new loan.

Real examples:

- HDFC Balance Transfer

- ICICI Personal Loan Balance Transfer

- Axis Bank Balance Transfer

- SBI Loan Transfer Facilities

Why it works well:

- Can reduce interest costs significantly.

- No need to create multiple new credit relationships.

- Often comes with top-up loan options.

Potential drawbacks:

- Less useful if you have several unrelated debts.

- Processing and switching charges can reduce savings.

Best for: People carrying a single expensive personal loan.

4. Fintech Lending Platforms (Use With Caution)

Many Indians first hear about debt consolidation through loan apps. Some are credible partners of licensed banks and NBFCs, while others primarily compete on speed and convenience.

Real examples:

- Paytm Personal Loans

- Moneyview

- KreditBee

- Navi

- CASHe

Advantages:

- Fast approvals.

- Digital application process.

- Convenient user experience.

Risks:

- Higher effective borrowing costs.

- Easier access may encourage more borrowing.

- Some borrowers focus on EMI rather than total repayment cost.

Best for: Borrowers who value speed and fully understand the loan terms before signing.

5. Loan Against Property (Best For Large Debt Consolidation)

This option is frequently overlooked.

If you own residential or commercial property and are dealing with substantial debt, a secured loan may be significantly cheaper than an unsecured personal loan.

Real examples:

- SBI Loan Against Property

- HDFC Loan Against Property

- ICICI Loan Against Property

- PNB Loan Against Property

- LIC Housing Finance LAP

Advantages:

- Lower interest rates.

- Larger loan amounts.

- Longer repayment periods.

Potential drawbacks:

- Property serves as collateral.

- Default carries serious consequences.

- Processing takes longer.

Best for: Borrowers carrying large debt balances who have strong repayment discipline.

Comparison Table: Which Source Is Best For Debt Consolidation?

| Source | Real Examples | Typical Interest Cost | Approval Difficulty | Speed | Best For |

|---|---|---|---|---|---|

| Public & Private Banks | SBI, HDFC Bank, ICICI Bank, Axis Bank | Usually lowest among unsecured options | High | Moderate | Salaried professionals with strong credit |

| NBFCs | Bajaj Finance, Tata Capital, Aditya Birla Finance | Moderate to high | Moderate | Fast | Self-employed borrowers and average credit profiles |

| Balance Transfer | HDFC, SBI, ICICI, Axis | Often cheaper than existing loan | Moderate | Moderate | One large loan or credit card balance |

| Fintech Lenders | Navi, Moneyview, KreditBee, Paytm Loans | Usually higher | Easier | Very Fast | Urgent requirements and digitally comfortable borrowers |

| Loan Against Property | SBI LAP, HDFC LAP, ICICI LAP | Usually lowest overall | Moderate | Slower | Very large debt burdens with property ownership |

FinanceTeam’s Honest Verdict

If your profile is strong enough, start with banks first. They usually provide the best balance of interest rate, borrower protection, and long-term affordability.

If a bank declines your application or you’re self-employed, NBFCs are often the next best choice.

Only consider fintech loan apps after comparing the total repayment amount, processing fee, foreclosure charges, and interest rate with traditional lenders.

For borrowers carrying several lakhs of high-interest debt and owning a property, a Loan Against Property can sometimes save substantially more interest than a standard debt consolidation loan, provided repayment remains disciplined.

The biggest mistake borrowers make is comparing only the EMI. The smartest borrowers compare the total amount payable over the entire loan tenure, because that’s where the real cost of debt consolidation becomes visible.

Key Takeaways

- A debt consolidation loan works by replacing several higher-rate debts with one lower-rate EMI. It restructures debt; it doesn’t erase it

- It’s most useful when a large share of your existing debt is high-cost, like credit cards

- RBI’s 2023–2025 rule changes mean approvals now lean more on verified income, not instant sign-ups

- The saving disappears fast if the old credit line stays open and gets used again

FAQs

There’s usually a small, short-term dip from the credit check and the new account. If you pay on time and don’t reopen old debt, most people see their score recover and then improve within a few months.

Yes, but expect closer scrutiny of bank statements and income proof than a few years ago. GST returns, e-invoice records, and consistent bank credits all help build a stronger case.

It depends on how many debts you’re carrying. A balance transfer involves moving one existing loan to a cheaper lender. Consolidation combines multiple debts, especially a mix of card dues and loans, into one.

Most lenders price their better rates for scores of 700 and above. Lower scores can still qualify, but usually at a rate closer to what you’re already paying, which weakens the point of consolidating.

It can cause a small, temporary dip because it shortens your credit history and lowers your total available limit. Most people find this trade-off worth it if the alternative is leaving temptation out in the open.

For a genuine emergency, maybe, in the very short term. But these products typically carry some of the highest effective costs in the lending market, precisely because they skip the checks that keep rates lower. They rarely make sense as a way to pay off existing debt.

Share this article: