- Bank Nifty Lot Size At A Glance

- What Does "Lot Size" Actually Mean?

- Why Does The Lot Size Keep Changing?

- Here's The Logic:

- A Timeline That Explains The Confusion

- What This Number Actually Costs You?

- Lot Size Is Not The Same As Margin

- Bank Nifty VS Nifty: Same Rules, Different Numbers

- Does Lot Size Affect Existing Positions?

- Should Beginners Trade Bank Nifty Derivatives?

- A Simple Framework Before You Place Your First Lot

- Where The Retail Story Fits In

- Key Takeaways

- Frequently Asked Questions

Bank Nifty Lot Size Explained: The Number That Decides How Much Money You Actually Need

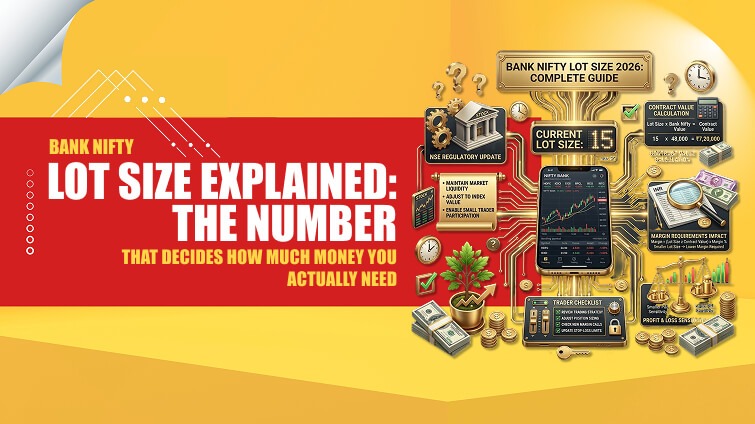

Bank Nifty lot size is the fixed number of index units bundled into one futures or options contract on the NSE.

Right now, that number is 30 units per lot. It matters because you can’t trade “one share” of an index. Simply put, you trade in lots, and the lot size decides your contract value, your margin, and how fast you can win or lose money.

If that sounds oddly specific for something so small, you’re not wrong to be curious. This one number has changed five times in three years.

Most explainers just tell you the current figure and move on. We’re going to do the opposite: walk through why it keeps moving, what it actually costs you, and where most first-time traders get it wrong.

Bank Nifty Lot Size At A Glance

| Detail | Current Value |

|---|---|

| Current lot size | 30 units per contract |

| Who sets it | NSE, under SEBI guidelines |

| Last revised | October 2025 circular, phased in through Jan–Mar 2026 |

| Applies to | Both futures and options contracts |

| Can it change again? | Yes, reviewed periodically as the index level moves |

| Where to verify | NSE’s official contract specification page |

Keep this table bookmarked. Lot sizes are not permanent, and the number above can be revised by the exchange without much public fanfare. Usually just a circular that traders find out about from their broker.

What Does “Lot Size” Actually Mean?

In equity trading, you can buy a single share of Reliance or HDFC Bank. Index derivatives don’t work that way. When you trade Bank Nifty futures or options, you’re buying or selling a fixed bundle of index units, and that bundle is the lot.

So if the lot size is 30, one Bank Nifty options contract represents 30 units of the index. You can’t trade 10 units or 45 units, only whole multiples of 30. This is why the phrase “buying one lot” and “buying one contract” mean the same thing in F&O trading.

Think of it like buying eggs. You buy a tray of 30. The price of the tray moves with the price of eggs. But you’re stuck buying in that fixed unit.

Why Does The Lot Size Keep Changing?

This is the part most articles skip, and it’s the part beginners actually need to understand.

SEBI, India’s market regulator, requires index derivative contracts to sit within a specific notional value band. Broadly between ₹15 lakh and ₹20 lakh per lot. Notional value just means lot size multiplied by the index price.

Here’s The Logic:

When Bank Nifty’s price rises, the value of a fixed lot rises with it. If the lot size stays the same while the index climbs, contracts start costing far more than the regulator wants. That pulls in more speculative money and pushes out smaller retail traders.

So NSE periodically resizes the lot to bring contract value back into that band. When the index cools off, or the lot value drifts too low, the reverse happens. And the lot size gets increased instead.

This isn’t random. It follows a defined process.

SEBI’s circular dated December 30, 2024, mandates these periodic reviews. And NSE calculates each new lot size using average closing index prices over a set review window before issuing its own circular.

A Timeline That Explains The Confusion

If you’ve read older blog posts, YouTube comments, or broker forums quoting different lot sizes, this table is why.

| Effective Date | Bank Nifty Lot Size | What Changed |

|---|---|---|

| Before June 2023 | 25 | Baseline lot size |

| June 30, 2023 | 15 | NSE reduced it to widen retail access |

| November 20, 2024 | 30 | SEBI raised the minimum contract value requirement to curb excess speculation |

| July 2025 expiry cycle | 35 | Index value rose; lot resized upward to stay within the value band |

| October 2025 circular (phased through Jan–Mar 2026) | 30 | Resized downward again as part of the scheduled review |

Notice the pattern. The number isn’t drifting in one direction. It moves up when the index value pushes contracts too small, and down when contracts get too expensive.

If you’re reading an old article, a forum post, or even an outdated calculator that says the lot size is 15 or 35, it was probably accurate the day it was written. It just isn’t anymore.

Always cross-check the figure against NSE’s live contract specifications before you place a trade.

What This Number Actually Costs You?

Numbers on a page don’t mean much until you attach a rupee figure to them. Here’s a simple scenario that plays out for many first-time index traders.

Say Bank Nifty is trading at 58,000. With a lot size of 30, one futures contract represents a notional value of:

58,000 × 30 = ₹17,40,000

That’s the exposure you’re controlling. Not the cash you need upfront.

You trade on margin, typically around 12–15% of the notional value for index futures, depending on your broker and prevailing volatility. In this example, that works out to roughly ₹2.1–2.6 lakh just to hold one futures lot.

This is where many newcomers stumble. They see “₹2 lakh margin” and assume that’s the maximum they can lose. It isn’t.

Margin is the entry ticket, not the ceiling on your loss. If Bank Nifty moves 500 points against your position, that’s 500 × 30 = ₹15,000 gone, regardless of how small your margin was.

This is the core idea behind leverage. You control a large position with a smaller deposit, and that cuts both ways.

This is also exactly why financial advisors keep repeating one line to beginners: understand your maximum loss before you understand your maximum gain.

Breaking a complex product like index derivatives into “what’s my exposure, what’s my margin, what’s my worst case” is a far more useful habit than chasing a single day’s profit potential.

And it’s a much simpler version of what a good financial advisor does when a client walks in wanting to trade something they don’t fully understand yet.

Lot Size Is Not The Same As Margin

These two get mixed up constantly, so it’s worth separating them clearly.

| Lot Size | Margin | |

|---|---|---|

| What it is | Fixed number of index units per contract | Cash/collateral required to hold the position |

| Who decides it | NSE (under SEBI guidelines) | Your broker, based on SPAN + exposure rules |

| How often it changes | Periodically, via exchange circular | Daily, based on market volatility |

| What it affects | Your contract value and P&L per point | How much capital you need to enter a trade |

| Can you control it | No, it’s fixed for all traders | Indirectly, via your broker’s leverage policy |

Lot size decides how big your bet is. Margin decides how much of your own money is tied up to place that bet. They move independently.

A lot size revision changes your contract value permanently, while your margin requirement can shift day to day depending on volatility.

Bank Nifty VS Nifty: Same Rules, Different Numbers

Since both indices follow the same SEBI framework, their lot sizes move on a similar logic. But the numbers themselves aren’t interchangeable.

As of the current cycle, Nifty 50’s lot size sits at 65, compared to Bank Nifty’s 30. Bank Nifty is a more volatile index by nature, since it’s concentrated in around a dozen banking stocks rather than fifty companies across sectors.

That concentration is part of why Bank Nifty options have historically attracted heavier day-trading volumes.

That means bigger, faster moves per point, packed into a smaller basket of stocks. It’s a meaningfully different risk profile from Nifty, even though the contract mechanics look identical on paper.

It’s also worth knowing that lot-sized index contracts aren’t unique to the NSE’s domestic market. Similar index derivative products are available to eligible investors through GIFT City.

It is India’s international financial hub, where contracts are dollar-denominated and follow their own separate specifications.

Again, that’s a detail that matters mainly to NRIs and global investors. But it’s a good example of how the same underlying idea scales across markets.

Does Lot Size Affect Existing Positions?

This trips people up every time NSE announces a revision.

New lot sizes generally apply to contracts entered into after the effective date. Typically starting with the nearest weekly expiry, then rolling into monthly, and finally quarterly and half-yearly contracts over the following weeks.

If you’re holding an existing position when a revision lands, your broker will usually ask you to adjust your position size to match the new lot multiple or square off the position before the transition deadline.

Miss that window, and your broker’s risk system may automatically square off the mismatched quantity. This is exactly the kind of detail that’s easy to miss if you’re new to F&O and only skimmed the headline number.

This is also where understanding Bank Nifty expiry day becomes genuinely useful rather than optional trivia. Lot size transitions are timed around expiry cycles.

Therefore, knowing which Thursday your contract actually expires and when the next lot-size-revised contract takes effect is the difference between calmly adjusting your position and scrambling at the last minute.

Should Beginners Trade Bank Nifty Derivatives?

Short answer: not as a first step into the markets, and definitely not with money you can’t afford to lose.

Bank Nifty options and futures are leveraged instruments built for traders who already understand position sizing, margin calls, and how fast losses can compound.

If you’re earning or investing for the first time, there’s a strong case for starting with the basics of how to start investing wisely. I would recommend:

- building an emergency fund

- understanding your risk appetite

- getting comfortable with simpler instruments before layering in leverage.

That doesn’t mean Bank Nifty derivatives are off-limits forever. It means sequencing matters.

Learn to size a position, understand what a speculative investment actually means versus a long-term holding, and only then consider derivatives with capital you’ve specifically set aside for higher-risk bets. But never your entire portfolio.

A Simple Framework Before You Place Your First Lot

- Build your base first. Have your emergency fund and core investments in place before touching derivatives.

- Define your maximum loss in rupees, not in “lots.” Decide the number before you open the trade, not after.

- Start with one lot. Don’t scale up until you’ve traded through at least a few full expiry cycles.

- Track margin and lot size separately. Both can change without warning. Check both before every trade, not just once when you opened your account.

- Review after every expiry. What worked, what didn’t, and whether your risk limit actually held. If you’re tracking multiple trades over time, calculating your actual annualised return using XIRR gives a far more honest picture of whether the strategy is working.

This is the same discipline that applies to how to diversify your investment portfolio. No single position, strategy, or index should be able to meaningfully dent your overall financial plan.

Where The Retail Story Fits In

Bank Nifty’s lot size revisions rarely make front-page news, but they quietly reshape retail participation each time they land. When the lot size was cut in 2023, smaller accounts found it easier to enter positions.

When SEBI’s 2024 mandate pushed contract values higher, a chunk of undercapitalized traders got priced out. Again, that was, in fact, the stated intent of the regulation, aimed at curbing speculative retail losses in F&O.

It’s worth remembering that institutional flows behave differently around these transitions too. Tracking FII and DII data around a lot size change can show whether bigger players are adjusting their hedges while retail traders are still figuring out the new contract math.

Large institutional players like mutual funds, insurance companies, and hedge funds mostly use Bank Nifty derivatives for hedging existing equity exposure rather than for directional bets.

A fund holding a large basket of banking stocks might use futures to offset short-term risk around a policy announcement.

A retail trader buying the same contract with no underlying holding is taking on a very different kind of risk, even though the instrument looks identical on the screen. Knowing who else is on the other side of your trade is a useful reality check before you place one.

Key Takeaways

- Bank Nifty’s current lot size is 30 units per contract.

- The exchange periodically revises it to keep the contract’s value within SEBI’s regulatory band.

- Lot size and margin are different things: one is fixed by the exchange, the other varies with your broker and market volatility.

- A revision usually applies to new contracts first; existing positions get a transition window.

- Always verify the live figure on NSE’s site or your broker’s app before placing a trade. Don’t trust an old blog post, including this one, without a quick cross-check.

Frequently Asked Questions

As of the latest NSE revision, the Bank Nifty lot size is 30 units per futures or options contract, applicable across weekly, monthly, and quarterly expiries following the phased rollout completed by March 2026.

NSE adjusts it periodically to keep each contract’s notional value within SEBI’s prescribed band, so contracts don’t become too cheap (encouraging excess speculation) or too expensive (shutting out legitimate retail participation).

Yes. Margin is typically calculated as a percentage of the contract’s notional value, so a change in lot size directly changes how much capital you need to hold a position, even if nothing else about the trade changes.

Yes, both futures and options contracts on Bank Nifty use the same lot size at any given time, since both are based on the same underlying index specification set by NSE.

Yes, but it typically applies to new contracts going forward. Existing positions usually get a transition window to adjust quantities or square off before the new lot size takes full effect.

They’re set independently based on each index’s price level and SEBI’s notional value band. So the numbers rarely match.

To clarify, the Nifty 50’s lot size is currently larger than the Bank Nifty’s despite both following the same regulatory logic.

NSE publishes current contract specifications, including lot size and quantity freeze limits, on its official derivatives page. That’s the most reliable source, more so than any third-party blog, including this one.

This article is for educational purposes only and does not constitute investment or trading advice. Lot sizes, margins, and contract specifications are subject to change by NSE and SEBI. Always verify current figures with your broker or NSE’s official circulars before trading..

Share this article: