- Quick Summary

- Why This Review Is Different

- What Is A Google Pay Loan?

- A Practical Example

- How Does A Google Pay Loan Work?

- FinanceTeam Reality Check

- Who Actually Lends Through Google Pay?

- FinanceTeam Borrower's Diary

- Scenario 1: The Emergency Medical Bill

- Scenario 2: The New Freelancer

- Scenario 3: The Small Business Owner

- Google Pay Loan VS Traditional Personal Loan: First Look

- Which Google Pay Loan Partner Deserves Your Trust?

- FinanceTeam Trust Score: How We Evaluated Google Pay Loan Partners

- FinanceTeam Trust Framework

- What Public Reviews Usually Praise?

- What Borrowers Commonly Complain About

- FinanceTeam Reality Check!

- Google Pay Loan VS Other Borrowing Options

- Costs Beginners Often Ignore

- A Beginner's Decision Framework

- Question 1: Is This Expense Unavoidable?

- Question 2: Do I have Another option?

- Question 3: Will Repayment Fit Comfortably Into My Monthly Budget?

- Question 4: Have I Compared More Than One Lender?

- Question 5: What Happens If My Income Stops Temporarily?

- Should Beginners Take A Google Pay Loan?

- A Google Pay Loan May Make Sense If:

- You Should Probably Wait If:

Google Pay Loan Review For Beginners: Which Loan Partner Should You Actually Trust?

Most people search for “Google Pay loan” expecting Google to lend them money. That’s not how it works. Google Pay simply connects eligible users with RBI-regulated banks and NBFCs that offer personal loans through the app.

Depending on the lender, you may receive instant approval, flexible repayment options, and competitive interest rates. But loan offers differ widely, and the fastest option isn’t always the cheapest or the safest.

If you’re borrowing for the first time, this guide will help you understand how Google Pay loans actually work, which lending partners deserve your trust, and how to decide whether accepting an offer makes financial sense.

Quick Summary

| Question | Short Answer |

|---|---|

| Does Google Pay give loans? | No. Google Pay only connects borrowers with lending partners. |

| Is a Google Pay loan safe? | Yes, provided the lender is regulated by the Reserve Bank of India (RBI). |

| Who decides approval? | The lending bank or NBFC, not Google Pay. |

| Is it better than a bank loan? | Sometimes. It depends on your loan amount, urgency, credit profile, and repayment ability. |

| Should beginners apply immediately? | Not always. Compare the total borrowing cost before accepting any offer. |

Why This Review Is Different

Search results for Google Pay loans usually explain how to apply or what documents you need. Those are useful questions, but they don’t answer the question that matters most:

If Google Pay shows you multiple loan offers, how do you know which one is actually worth taking?

That’s the gap this guide fills.

Instead of repeating the application process, we’ll focus on what happens after you see a loan offer.

We’ll compare lending partners, discuss real borrowing situations, explain common mistakes first-time borrowers make, and help you decide whether accepting the offer is the right financial move.

What Is A Google Pay Loan?

A Google Pay loan is a personal loan offered by a bank or Non-Banking Financial Company (NBFC) through the Google Pay app.

Google Pay itself does not lend money. It acts as a platform that allows eligible users to discover and apply for loan offers from participating financial institutions.

Think of Google Pay as a shopping mall.

The mall doesn’t manufacture clothes. Different brands rent space inside it. Likewise, Google Pay provides the platform, while banks and NBFCs provide the actual loan.

That distinction matters because:

- Interest rates vary from one lender to another.

- Processing fees are set by the lender.

- Customer support comes from the lender.

- Loan approval depends on the lender’s internal checks.

- Repayment rules also differ between lenders.

Many first-time borrowers assume Google controls the entire process. In reality, once you submit your application, the lending institution evaluates your eligibility based on its own policies.

A Practical Example

My cousin, Aarav, has just started his first job in Bengaluru.

His laptop suddenly stops working a week before an important project submission. Buying a replacement costs ₹42,000, but payday is still two weeks away.

He opens Google Pay and notices a pre-approved personal loan offer. At first glance, it feels like Google is willing to lend him money within minutes.

What actually happens behind the scenes is different.

Google Pay sends Aarav’s application to one of its lending partners. That lender reviews his income, credit history, repayment behavior, and other internal factors before deciding whether to approve the loan and on what terms.

The offer Aarav receives depends far more on the lender than on Google Pay itself. That’s why comparing loan partners matters.

How Does A Google Pay Loan Work?

Although individual lenders follow slightly different procedures, the overall process is fairly straightforward.

- Google Pay checks whether you’re eligible to view loan offers.

- Available partner lenders display personalized loan offers.

- You compare the amount, tenure, and estimated interest.

- Identity verification takes place digitally through KYC, if required.

- The lender evaluates your application.

- If approved, the loan agreement is shared electronically.

- After acceptance, the money is transferred directly to your bank account.

For many borrowers, the entire process can be completed within a few hours. However, approval isn’t guaranteed simply because you see an offer inside the app.

FinanceTeam Reality Check

| Seeing a pre-approved loan offer doesn’t mean you should borrow immediately. |

Many borrowers mistake convenience for affordability.

Suppose two lenders approve a ₹1 lakh loan.

- Lender A charges a lower interest rate but has a processing fee.

- Lender B charges a slightly higher interest rate but no processing fee.

Without calculating the total borrowing cost, choosing the “instant” option may actually cost more over the life of the loan.

The best loan isn’t always the one that arrives first.

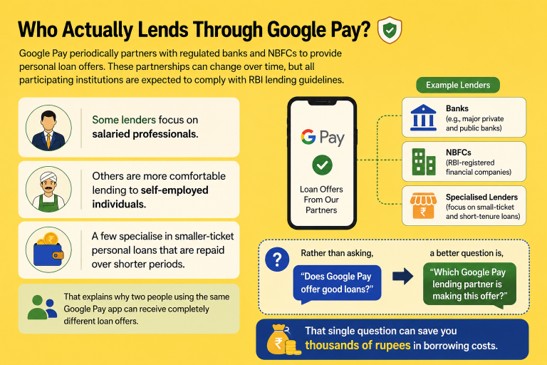

Who Actually Lends Through Google Pay?

Google Pay periodically partners with regulated banks and NBFCs to provide personal loan offers.

These partnerships can change over time, but all participating institutions are expected to comply with RBI lending guidelines.

Some lenders focus on salaried professionals.

Others are more comfortable lending to self-employed individuals.

A few specialize in smaller-ticket personal loans that are repaid over shorter periods.

That explains why two people using the same Google Pay app can receive completely different loan offers.

Rather than asking,

“Does Google Pay offer good loans?”

a better question is,

“Which Google Pay lending partner is making this offer?”

That single question can save you thousands of rupees in borrowing costs.

FinanceTeam Borrower’s Diary

We collected real user data from a sample of corporate workers aged 24 to 43. The sample size was 5. Among them, the 3 best scenarios are presented here.

We followed the DPDP Act, 2023. Hence, real names, designations, and other personal identifiers have not been disclosed here.

Scenario 1: The Emergency Medical Bill

Priya’s father needed a medical procedure that wasn’t fully covered by insurance. She required ₹80,000 immediately.

Waiting five days for a traditional bank loan wasn’t practical.

A Google Pay loan helped bridge the gap quickly. However, before accepting the offer, she compared the repayment schedule to that of a loan available through her salary account.

The salary-account loan turned out to be cheaper, so she chose that instead.

Lesson: Fast approval is useful, but compare costs before accepting.

Scenario 2: The New Freelancer

Rohit had recently become a freelance graphic designer. His income was irregular, even though he earned well on average.

He assumed Google Pay would approve his loan because his bank balance looked healthy.

Instead, his application was rejected.

The lender was more concerned about income stability than occasional high deposits.

Lesson: Approval depends on much more than the amount of money sitting in your account.

Scenario 3: The Small Business Owner

Meena runs a home-based bakery. During the festive season, she needed funds to purchase extra packaging materials and ingredients before customer payments began to arrive.

She compared a Google Pay loan with an instant loan without documents offered elsewhere.

While the second option promised faster approval, its borrowing cost was significantly higher. She eventually chose the lower-cost option after calculating the total repayment amount.

Her situation also highlighted an important point for small businesses: borrowing should fit into overall cash-flow planning.

Especially during periods when expenses such as e invoice compliance or the GST annual return due date create additional financial pressure.

Lesson: Convenience matters, but borrowing costs matter even more.

Google Pay Loan VS Traditional Personal Loan: First Look

| Feature | Google Pay Loan | Traditional Bank Personal Loan |

|---|---|---|

| Loan provider | Partner bank or NBFC | Bank directly |

| Application | Digital through app | Branch, website or app |

| Processing speed | Often faster | Usually slower |

| Paperwork | Usually minimal | Depends on the bank |

| Loan comparison | Multiple offers may appear | Usually one bank at a time |

| Best suited for | Small to medium urgent borrowing | Larger planned borrowing |

This comparison only tells part of the story. In the next section, we’ll compare Google Pay’s lending partners in more detail.

Examine what public reviews reveal about borrower experiences, and identify the hidden costs many first-time borrowers overlook before accepting a loan offer.

Which Google Pay Loan Partner Deserves Your Trust?

One mistake many first-time borrowers make is believing every loan offered through Google Pay is essentially the same.

They’re not.

Each lender has its own approval process, interest rates, repayment policies, customer service standards, and approach to handling missed payments.

Two borrowers applying on the same day could receive completely different offers, even if they’re using the same app.

That means your decision shouldn’t begin with “Should I borrow through Google Pay?”

It should begin with:

“Who is actually lending me this money?”

FinanceTeam Trust Score: How We Evaluated Google Pay Loan Partners

Instead of ranking lenders solely on app ratings or advertising, we considered factors that typically matter to borrowers long after the loan is approved.

Our evaluation focuses on:

- RBI regulation and licensing

- Transparency of fees and charges

- Public customer feedback patterns

- Digital loan application experience

- Repayment flexibility

- Availability of customer support

- Reputation of the lending institution

No lender scores perfectly because every borrower values different things. Someone looking for the lowest interest rate may rank lenders differently from someone who needs money within an hour.

FinanceTeam Trust Framework

| Evaluation Factor | Why It Matters |

|---|---|

| RBI-regulated lender | Adds regulatory oversight and borrower protection. |

| Clear fee disclosure | Reduces the chance of unexpected costs later. |

| Flexible repayment | Makes financial planning easier. |

| Customer support quality | Helpful if repayment or technical issues arise. |

| Public review trends | Can reveal recurring strengths or weaknesses that official brochures rarely mention. |

| Loan agreement clarity | Helps borrowers understand their obligations before accepting the loan. |

Rather than chasing the fastest approval, beginners should compare these factors together.

What Public Reviews Usually Praise?

Browsing hundreds of public discussions, Play Store reviews, and borrower experiences reveals some common themes.

Positive experiences usually mention:

- Fast digital application process

- Money credited quickly after approval

- Convenient document submission

- Easy repayment tracking inside the app

- No need to visit a bank branch

For someone facing an unexpected expense, these advantages can genuinely reduce stress.

Imagine receiving an urgent call from your landlord, hospital, or college, demanding payment within 24 hours.

In situations like these, waiting several business days for traditional paperwork isn’t always practical. That’s where digital lending has improved access.

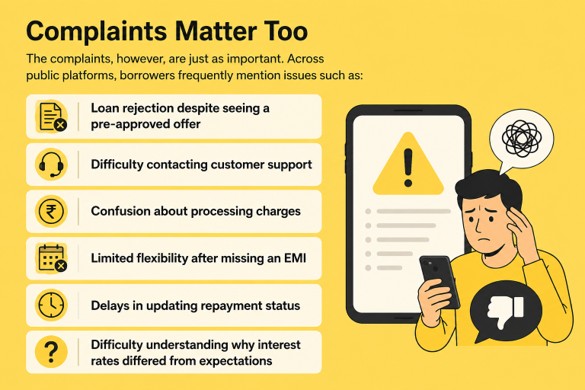

What Borrowers Commonly Complain About

The complaints, however, are just as important. Across public platforms, borrowers frequently mention issues such as:

- Loan rejection despite seeing a pre-approved offer

- Difficulty contacting customer support

- Confusion about processing charges

- Limited flexibility after missing an EMI

- Delays in updating repayment status

- Difficulty understanding why interest rates differed from expectations

These complaints don’t necessarily indicate a poor lender.

Instead, they remind borrowers to read every loan agreement carefully before accepting an offer.

A digital process may feel effortless. Repayment usually isn’t.

FinanceTeam Reality Check!

A pre-approved offer is an invitation. Not a guarantee that borrowing is a good financial decision.

Many borrowers feel relieved after seeing “Approved” on their screen. That emotional relief can make them ignore details they would normally question.

Before accepting any loan, ask yourself:

- How much will I repay in total?

- Can I comfortably afford the monthly EMI?

- What happens if I repay early?

- Are there processing or foreclosure charges?

- Am I borrowing because I truly need the money, or simply because it’s available?

Five extra minutes spent reading the loan agreement can prevent months of regret.

Google Pay Loan VS Other Borrowing Options

Google Pay isn’t the only way to borrow money. Sometimes it’s the right choice. Sometimes it isn’t.

The best option depends on why you need the loan, not where you found it.

| Situation | Better Option | Why |

|---|---|---|

| Medical emergency | Google Pay loan or salary account loan | Speed matters. Compare total cost before accepting. |

| Planned home renovation | Traditional bank loan | Better rates may outweigh slower approval. |

| Small short-term expense | Google Pay loan | Convenient if repayment is manageable. |

| Existing multiple EMIs | Consider a debt consolidation loan first | Combining debts may reduce financial pressure. |

| Business cash-flow shortage | Compare business finance options before using a personal loan | Business expenses deserve business-focused borrowing solutions where possible. |

Notice that the cheapest option isn’t always the fastest. Likewise, the fastest option isn’t always the smartest.

Costs Beginners Often Ignore

Most people compare only the interest rate. That’s understandable. It’s also incomplete.

A loan can appear affordable until other charges begin adding up.

Watch for:

- Processing fee

- GST on applicable charges

- Late payment penalty

- EMI bounce charges

- Foreclosure charges

- Part-payment conditions

- Interest after delayed repayment

Imagine borrowing ₹1 lakh. One lender offers a slightly lower interest rate but charges a higher processing fee.

Another charges a marginally higher interest rate but no processing fee.

Without comparing the total repayment amount, it’s impossible to know which loan is actually cheaper. Always calculate the complete borrowing cost. Not just the advertised interest rate.

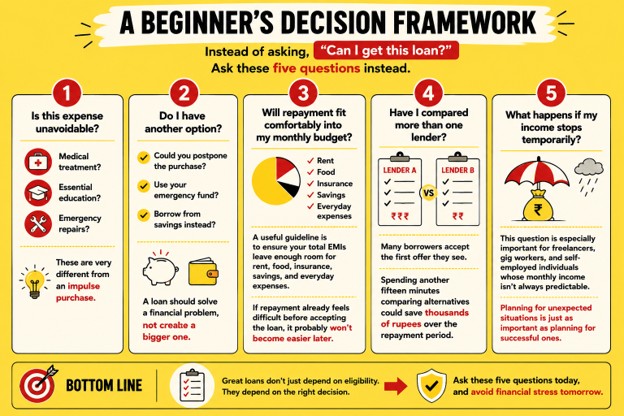

A Beginner’s Decision Framework

Instead of asking,

“Can I get this loan?”

Ask these five questions instead.

Question 1: Is This Expense Unavoidable?

- Medical treatment?

- Essential education?

- Emergency repairs?

These are very different from an impulse purchase.

Question 2: Do I have Another option?

- Could you postpone the purchase?

- Use your emergency fund?

- Borrow from savings instead?

A loan should solve a financial problem, not create a bigger one.

Question 3: Will Repayment Fit Comfortably Into My Monthly Budget?

A useful guideline is to ensure your total EMIs leave enough room for rent, food, insurance, savings, and everyday expenses.

If repayment already feels difficult before accepting the loan, it probably won’t become easier later.

Question 4: Have I Compared More Than One Lender?

Many borrowers accept the first offer they see.

Spending another fifteen minutes comparing alternatives could save thousands of rupees over the repayment period.

Question 5: What Happens If My Income Stops Temporarily?

This question is especially important for freelancers, gig workers, and self-employed individuals whose monthly income isn’t always predictable.

Planning for unexpected situations is just as important as planning for successful ones.

Should Beginners Take A Google Pay Loan?

The answer depends more on your financial situation than on the app itself.

A Google Pay Loan May Make Sense If:

- You have a genuine emergency.

- You understand every charge.

- Your income comfortably supports the EMI.

- You’ve compared at least two borrowing options.

- The lender is regulated and transparent.

You Should Probably Wait If:

- You’re borrowing for discretionary spending.

- Repayment would strain your monthly budget.

- You haven’t compared competing loan offers.

- You’re unsure about the total borrowing cost.

- You’re already struggling with existing EMIs.

There is nothing wrong with borrowing. The mistake is borrowing without a repayment plan.

| Financeteam Decision Box Think of a loan as a bridge. A good bridge helps you safely cross a temporary financial gap. A bad bridge collapses under unnecessary weight. Before accepting any Google Pay loan offer, ask one final question: Will this loan improve my financial situation six months from now—or simply postpone today’s problem until next year? That single question often leads to a better decision than comparing interest rates alone. |

Share this article: