- Quick Summary Box

- Table 1: Complete GST Rate Matrix Across All Insurance Products

- The Real Characteristics Of GST On Insurance Premium

- The Invisible Trade-Offs: Pros & Cons Of The Current Tax Regime

- The Advantages

- The Disadvantages

- The FinanceTeam "Tax Mitigation" Decision Framework

- The Small Business Loophole: Input Tax Credit (ITC)

- Table 2: Input Tax Credit Eligibility Rules for Indian Enterprises

- Reality Check

- Cross-Industry Reality Checks: How 18% Alters Buying Behavior

- Frequently Asked Questions (FAQs)

- Core Definition Queries

- Small Business & ITC Queries

- Consumer Optimization Queries

- Official GST Utility Desk: Portals, Filings, & Verification

- The Core Compliance Portals

- Direct Action Links & Taxpayer Tools

GST On Insurance Premium: The Hidden Cost In Your Policy And How To Avoid Overpaying

GST on insurance premium is a mandatory indirect tax levied by the Government of India on the purchase and renewal of insurance policies. It involves a fixed percentage tax added directly to your base premium amount.

It offers a structured way for the state to collect revenue from service consumption but carries the risk of increasing out-of-pocket insurance costs for retail buyers who cannot claim input tax credits.

Quick Summary Box

- GST is unavoidable: Every commercial insurance policy in India attracts GST, ranging from 18% down to 0% for specific government welfare schemes.

- Term Insurance Hit: Pure term plans, which beginners use to secure their family’s financial future, carry the highest absolute tax burden with no maturity returns.

- Tax Saving Misconception: While Section 80D allows deductions for your health insurance premium, the GST component itself does not yield additional compounding tax breaks.

- Corporate Hack: If you operate a small business, you can legally claim Input Tax Credit (ITC) to eliminate this cost entirely on specific commercial policies.

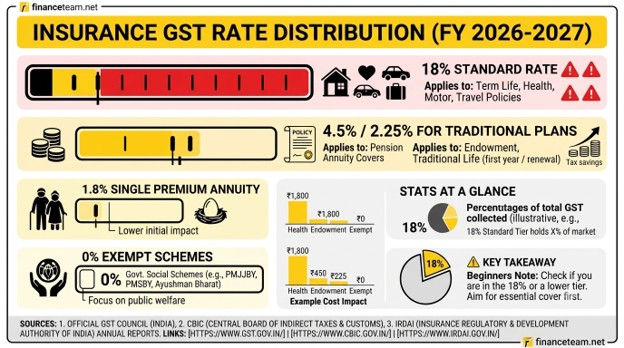

Table 1: Complete GST Rate Matrix Across All Insurance Products

| Insurance Category | Base Type | GST Rate | Real-World Impact per ₹10,000 Base Premium | Who Pays It? |

|---|---|---|---|---|

| Term Insurance | Pure Risk Cover | 18% | ₹1,800 | Retail Consumer |

| Health Insurance | Individual / Family Floater | 18% | ₹1,800 | Retail Consumer |

| Motor Insurance | Third Party & Own Damage | 18% | ₹1,800 | Vehicle Owner |

| Endowment Plans | 1st Year Premium | 4.5% | ₹450 | Investor / Saver |

| Endowment Plans | Renewal Years | 2.25% | ₹225 | Investor / Saver |

| Single Premium Annuity | Pension Purchase | 1.8% | ₹180 | Retiree |

| Govt. Social Schemes | PMJJBY / PMSBY | 0% | ₹0 | Lower Income Group |

What Beginners Misunderstand: The “Hidden Tax” Trap

When Aman, my younger brother, turned 23 and landed his first job in Bengaluru, he decided to buy a term insurance policy worth ₹1 Crore.

The aggregator website quoted a clean, attractive premium of ₹10,000 per year. Aman swiped his credit card, only to see the final deduction statement show ₹11,800. He assumed it was an unlisted processing fee or platform convenience charge.

It wasn’t. It was the 18% standard rate applied to financial protection services in India.

Beginners often focus solely on base premiums when budgeting for long-term protection assets. Over a 30-year term policy lifecycle, that single blind spot means Aman will pay ₹54,000 purely in non-refundable taxes.

Financial advisors recommend tracking these outlays meticulously because, unlike the base investment component, the tax slice does not compound with returns.

The Real Characteristics Of GST On Insurance Premium

- Regressive Application: The tax rate remains exactly the same whether your monthly income is ₹25,000 or ₹2,500,000.

- No Investment Trajectory: The money goes straight to the exchequer; it does not earn bonuses or stock market dividends inside Unit Linked Insurance Plans (ULIPs).

- Dynamic Regulatory Linkage: Rates are determined strictly by the GST Council meetings and are subject to amendments independent of your long-term lock-in contract terms with the insurer.

The Invisible Trade-Offs: Pros & Cons Of The Current Tax Regime

If you fall under the current tax regime, this section is for you:

The Advantages

- Systemic Compliance Transparency: The integration of the corporate supply chain via an active e invoice mechanism ensures that insurance companies cannot obscure hidden administrative charges under the guise of statutory taxes.

- Subsidized Public Welfare: The high tax revenue collected from premium commercial covers enables the state to run zero-tax baseline protection initiatives such as the Pradhan Mantri Suraksha Bima Yojana for economically vulnerable citizens.

The Disadvantages

- Barriers to Essential Medical Entry: Levying 18% on health insurance premiums acts as a direct financial disincentive for families attempting to purchase comprehensive private medical buffers.

- Distorted Yield Matrices: In savings-cum-insurance vehicles, the front-loaded tax deductions erode the primary principal amount before it ever hits the investment fund basket, permanently lowering your ultimate net portfolio yield.

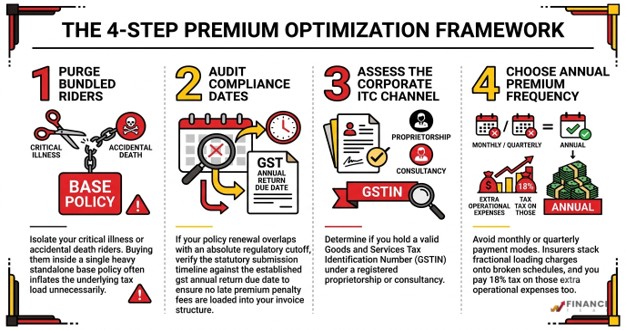

The FinanceTeam “Tax Mitigation” Decision Framework

If you are a salaried individual or a first-time investor stepping into the insurance ecosystem, use this structured four-step path to optimize what you shell out.

The Small Business Loophole: Input Tax Credit (ITC)

If you are a freelancer, a digital creator, or a small business enterprise with an active GSTIN, you do not have to absorb this 18% tax hit as an outright expense.

Table 2: Input Tax Credit Eligibility Rules for Indian Enterprises

| Insurance Variant | Insurance Variant | ITC Eligibility | ITC Eligibility |

|---|---|---|---|

| Group Health Insurance | Employee Benefit (Statutory Mandate) | Fully Eligible | Must be required by labor laws or corporate policy to protect staff. |

| Commercial Vehicle Cover | Goods Transportation / Delivery | Fully Eligible | Vehicle must be registered strictly under the business name. |

| Keyman Insurance | Protecting Vital Directors / Partners | Fully Eligible | Premium must be fully funded from the company’s operating books. |

| Personal Health Plan | Individual Self-Use Policy | Strictly Ineligible | Cannot be claimed against business revenue accounts. |

| Personal Car Policy | Commuting from Home to Office | Strictly Ineligible | Considered a personal consumption asset by audit authorities. |

When an enterprise claims this tax back during their routine monthly filings, it creates an internal GSTR-9 tax reconciliation loop in which the tax paid on incoming insurance and utility services directly offsets output liability on sales.

Reality Check

A common piece of advice shared on social media is that you can buy a personal luxury car, insure it, and claim 18% ITC simply by using your company’s GSTIN. In reality, Tax departments aggressively flag these filings during audits. If the asset cannot be conclusively linked to core business revenue generation operations, the claim is rejected, and hefty penalties are applied retroactively.

Cross-Industry Reality Checks: How 18% Alters Buying Behavior

To appreciate the scale of 18% on an essential safety net item, consider how standard daily services are taxed under the unified indirect framework.

If you walk into an eatery, your billing relies on a structured restaurant gst rate, which sits comfortably at 5% because food consumption is designated as a baseline core necessity. Similarly, booking budget accommodation involves navigating a modest hotel gst rate tier tailored to support tourism velocity.

Yet, when an ordinary individual attempts to isolate their family from catastrophic medical bankruptcy or premature mortality events, the system applies a heavy 18% slab. The same bracket reserved for lifestyle items.

This structural anomaly means that consumers must be incredibly deliberate with policy configurations to prevent structural premium bleed from compromising their household liquidity positions.

Frequently Asked Questions (FAQs)

People querying about GST on insurance premium usually ask these. We have divided the queries based on type and intent:

Core Definition Queries

Yes. Every standard commercial insurance policy issued by state-owned or private corporations in India automatically attracts GST at the time of calculation. The insurer acts as a collection agent, meaning the buyer cannot opt out of this component during the regular point-of-sale checkout sequence.

Yes. Under Section 80C for life insurance and Section 80D for health insurance, the total premium amount you actually pay is eligible for deduction calculations, subject to the maximum investment limits set by the prevailing Income Tax Act.

Small Business & ITC Queries

You must ensure the insurer prints your exact legal business entity name, along with your verified corporate GSTIN, directly on the face of the tax invoice. The transaction flow must match the systematic ledger reflections visible inside your internal e-filing portal balances.

If the primary service provider fails to reflect the policy invoice correctly, the credit block will not populate inside your electronic accounts. This disrupts your standard corporate financial audit loops and forces manual reconciliations during the concluding processing cycles of the financial year.

Consumer Optimization Queries

No. In a Unit Linked Insurance Plan (ULIP), the 18% standard rate applies exclusively to the modular expenses allocated to internal management fees, operational administration, and mortality risk underwriting, rather than to the entire pool of your core asset investment principal.

No. The baseline service tax structure remains fixed at 18% across all standard private health and retail life covers, regardless of the policyholder’s age bracket or demographic status.

Official GST Utility Desk: Portals, Filings, & Verification

When you are managing your policy invoices, running an enterprise, or reconciling your tax inputs, relying on third-party aggregators can lead to costly operational compliance errors.

Use these direct, official Government of India channels to manage your filings and verify tax authenticity, while calculating gst on insurance premium:

The Core Compliance Portals

- Official GST Council Secretariat Portal

- What it’s for: Track official amendments, rate change notifications, and press releases directly from the decision-making body that sets the tax slabs on insurance premiums and other commercial goods.

- Official Government GST Common Portal

- What it’s for: This is your primary engine for all statutory monthly and quarterly actions. Use this dashboard to log in, file your regular financial returns, and review your electronic ledgers.

- Official e-Invoice Production Portal

- What it’s for: For business owners verifying corporate policies, this portal lets you track and authenticate structured invoice registrations generated by enterprise supply networks.

Direct Action Links & Taxpayer Tools

- Search Taxpayer by GSTIN / UIN

- What it’s for: Enter an insurance company’s or a vendor’s tax identification number to confirm their active registration status and ensure your Input Tax Credit (ITC) path flows without manual bottlenecks.

- Verify e-Invoice via Invoice Reference Number (IRN)

- What it’s for: Protect your business from fraudulent billings. Enter the unique string or scan the QR code on your insurance policy to check whether the document is recognized by the centralized network.

- Track GST Return Filing Status

What it’s for: Keep tabs on whether your financial providers or business entities have uploaded their data on time, protecting your monthly cash positions from compliance delays.

Share this article: