- What Does Unclaimed Deposits Mean?

- Funds Which Can Turn Into “Unclaimed”

- What Makes Your Money Go Into The List Of “Unclaimed”?

- What Happens To The Unclaimed Deposits?

- How Does Someone Verify Unclaimed Deposits On The Udgam Portal?

- 1. Register For The Udgam Portal

- 2. Log In To Your Personal Account

- 3. Search For Deposits That Are Unclaimed

- Banks Which Are Available On The Udgam Portal

- How Can Someone Ignore Unclaimed Deposits?

- What Should We Keep In Mind About The Udgam Portal?

Unclaimed Deposits: How To Check On The RBI Udgam Portal And Claim Your Bank Deposit Money?

Sometimes people can’t remember about the old bank accounts or about the fixed deposits they opened many years ago.

So the money stays as it is in the account, unused. These are called “unclaimed deposits” by banks, but the money belongs to the owner, not to the bank.

By December 2025, there will be a huge amount of forgotten money in Indian Banks, but many people can claim it by looking at their old accounts and records.

In this article, we will learn how to access the unclaimed deposits through the Udgam portal.

What Does Unclaimed Deposits Mean?

Unclaimed deposit days in the bank account that haven’t been used for more than a decade.

Actually, they are kind of different from dormant accounts, which become fully inactive after 2 years with zero activity. But it can still be used or reactivated easily by the account holder.

Funds Which Can Turn Into “Unclaimed”

Many types of unused bank-related money sometimes become unclaimed deposits.

Like money in savings or fixed deposit accounts, unused loan or security deposits, pending cheques or transfers, unused card balances (prepaid), and even converted deposits of foreign money.

Hence, there are other similar amounts identified by the Reserve Bank of India that might be counted in the category if they are not used for a long time.

What Makes Your Money Go Into The List Of “Unclaimed”?

The money becomes unclaimed, especially when people don’t remember their old accounts.

Or sometimes don’t know about family members’ accounts.

Hence, sometimes the change of contact details or face name mismatches as well, or there is confusion when the bank mergers occur.

And with no active transactions for a long time, the bank recognizes these accounts as inactive.

What Happens To The Unclaimed Deposits?

An unclaimed bank account and the money that has been in the account don’t mean that the money is lost.

However, after a certain period, the authorities move the money to a special fund called the Depositor Education and Awareness (DEA) Fund. Reserve Bank of India (RBI) manages this fund.

But still, the money belongs to you. The bank cannot use this money by itself, so you can claim it anytime you want with the proper proof of ownership.

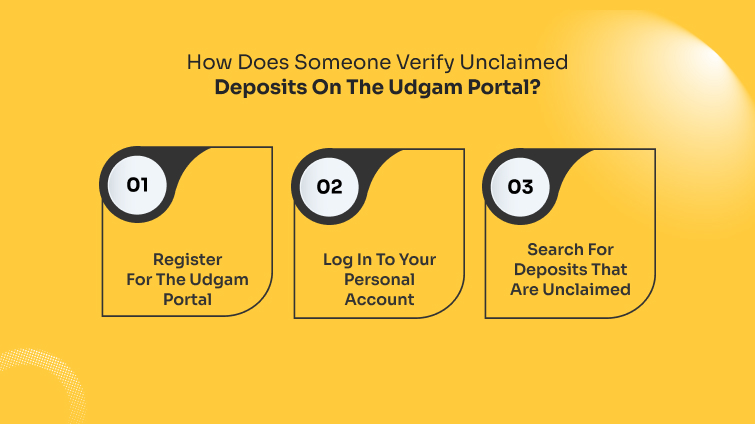

How Does Someone Verify Unclaimed Deposits On The Udgam Portal?

Here are the main ways to verify unclaimed deposits on the Udgam Portal.

1. Register For The Udgam Portal

Go to the portal of UDGAM. Then click the register button and type your name and mobile number.

Create a password as well, fill in the captcha, and agree to the mentioned disclaimer. At the end, verify it using the OTP.

2. Log In To Your Personal Account

Type your personal mobile number, captcha, and password there. Then verify your account with an OTP to access it.

3. Search For Deposits That Are Unclaimed

Enter the name of the account holder and choose the bank. You have to provide one detail like PAN, driving license number, voter ID, birth date, or passport number.

Then click the search button to check whether any enclave deposits are available. And there will definitely be a procedure to claim it.

Banks Which Are Available On The Udgam Portal

This portal allows searching across 30 major banks in India. Hence, the list of banks is given below:

- Bank of India

- Axis Bank Ltd.

- Bank of Maharashtra

- Central Bank of India

- Canara Bank

- Bank of Baroda

- Federal Bank Ltd

- DBS Bank India Ltd.

- Dhanlaxmi Bank Ltd.

- HDFC Bank Ltd.

- HSBC Ltd.

- ICICI Bank Ltd.

- Indian Overseas Bank

- IDBI Bank Ltd.

- Indian Bank

- Jammu & Kashmir Bank Ltd.

- IndusInd Bank Ltd

- Karnataka Bank Ltd.

- Karur Vysya Bank Ltd.

- Kotak Mahindra Bank Ltd.

- Saraswat Cooperative Bank Ltd

- Punjab National Bank

- South Indian Bank Lt

- Punjab and Sind Bank.

- Standard Chartered Bank

- State Bank of India

- Tamilnad Mercantile Bank Ltd.

- UCO Bank

- Union Bank of India

How Can Someone Ignore Unclaimed Deposits?

You must keep at least one of your accounts and investments written along with the details of bank accounts, fixed deposits, policies, and other investments.

Hence, you should close the unused and duplicate accounts to clear up all the confusion.

Add a nominee to all your bank accounts so that your money can easily reach your family in an emergency.

You should use your account at least once a year, even if it’s just a small transaction. Because it will help you ensure your account is active.

In addition to this, you should update your details related to KYC regularly. Inform the bank if you change your phone number or address.

Have a look at your account regularly via mobile or internet banking. Regular checking helps you stay aware of your exact balance.

Thus, you can review your accounts once a year. A simple early check helps to keep everything active and traceable.

Even if the money becomes unclaimed and the accounts become inactive, that doesn’t mean that your money has disappeared or been lost.

You can still find the money and claim it by using tools like the UDGAM portal of the Reserve Bank of India (RBI) and with the right documents.

What Should We Keep In Mind About The Udgam Portal?

If you are unable to find your fixed deposit receipt, go ahead and visit your bank’s branch. Hence, always carry your ID.

Always share any details you remember, like the amount, approximate date, or branch name, so they can trace it and help you properly.

Often, the bank gets merged, or the branch is closed, so tell the bank the previous name of the older branch or code.

Hence, submit a re-KYC when needed, and request that they issue a statement or confirmation of the interest and balance.

As a result, the account holder often passes away. Hence, you should always provide the bank with the information immediately and submit the certificate of death and your KYC at the earliest.

The account often has a superior option. As a result, the living holder or the nominee can generally claim the money with basic documentation.

Share this article: